Publications

- Category: Infrastructure and energy

Liliam F. Yoshikawa, Carolina de Almeida Castelo Branco and Camila de Carli Rosellini

A new resolution of the National Mining Agency (ANM) that provides for rules regarding the Mine Closure Plan (PFM) was issued on April 30, 2021 and will enter into force on June 1, 2021. Resolution ANM No. 68/2021 presents provisions to standardize and regulate the set of procedures necessary for the monitoring of PFM throughout the life of the mine, as well as the decommissioning process of mining enterprises and post use of such areas.

Every mining enterprise, whether in force and in operation or with its activities to be initiated or suspended, must present a PFM prepared by a legally qualified professional and accompanied by the respective Technical Responsibility Note (ART).

These measures shall be complied with within certain deadlines that vary from 12 months, as of the publication of the resolution, up to 24 months from 1st june 2021, when the new rules will enter into force.

Operating mining enterprises in mining concession phase must present an updated PFM by May 4, 2021. In turn, those in mining concession request phase must submit the updated PFM within 180 days, as of the mining concession grant.

The elements that must necessarily make up the MPF to be submitted to the ANM vary according to the life phase of the mine and the start of its activities.

For projects that have just reached mining concession phase or those in the mining concession request phase which effective mining activity have not yet been initiated, the elements that should be included in the plan include:

- Maps, plants, photographs and images (standardized according to the standards of ABNT - Brazilian Association of Technical Standards);

- Documentation describing the current situation of the area;

- Mining infrastructure project overlaid to the current context of the area;

- Conceptual design of decommissioning of civil structures and physical and chemical stabilization of the remaining structures;

- The rehabilitation actions of the area already performed;

- Main monitoring and maintenance actions already planned in the area; and

- Physical-financial schedule of pfm, integrating pre-closing, closing and post-closing actions.

In the case of mines in exhaustion closure, in addition to the same elements for projects in the application phase or mining concession with activity not initiated, the PFM should contain:

- Characterization of the area of the enterprise, with data from civil structures, geotechniques, hydraulics, electrical installations, equipment, among others (standardized according to ABNT standards);

- Assessment of the risks arising from the closing of the enterprise and ways of mitigating any damages resulting from the activity;

- Plan for the demobilization of the facilities and equipment that make up the infrastructure of the enterprise;

- measures to prevent unauthorised access to facilities and to prohibit access to hazardous areas;

- Maintenance actions and monitoring of the remaining structures after the closure of the project; and

- Guidelines for adequacy of the area to the predicted future use.

For mines that are closed before exhaustion, the PFM must contain:

- Declaration of remaining mineral resources and reserves and

- Technical and economic justification for the closure of mining activities.

Finally, for operational mines, all previous elements and the life expectancy of the enterprise will be required.

In the case of projects containing mining tailing dams, the PFM should have, as a mandatory element, the tailing dam decharacterization plan or other technical solution in charge of the technical responsible, with the objective of reducing the Associated Potential Damage (DPA)[1] to each existing tailing dam.

If it is not possible to mischaracterize the tailing dam, the PFM should provide for its monitoring in accordance with current legislation. In such cases, for the preparation of the PFM, the professional responsible for the plan must be legally qualified to provide services related to tailing dams and present the respective ART.

Just as the mining activity itself and the consequent useful life of a mine are subject to variations that depend on various economic and climatic factors, the PFM should also be updated to be consistent with such changes. In this sense, the rule was inserted that the PFM should be updated every five years or at the time of updating the Economic Recovery Plan (PAE), the one that occurs first. Exception is made in the case of undertakings with mining assets with validity of less than five years and/or with the expected closure of mining activities of less than two years. In the latter case, it is mandatory to prove the execution of the PFM.

In addition to the elements mentioned above for each case, depending on the life phase of the mine, pfm updates should include:

- Description of the closing actions of the areas that may be closed throughout the operation (in the case of progressive closure) and

- Updated planialtimetric survey of the areas and structures that make up the enterprise.

Such updates shall be reported to the ANM within the deadlines set out above and be available at the mine in case of inspections.

The latest PFM update should be communicated to the ANM at least two years before the expected mining closure and, in case it takes place before exhaustion, the updated PFM should be presented. In the same sense, the waiver of the mining title may only be approved after approval by the ANM of the final report of implementation of the PFM.

Small enterprises, with proven mining and processing operations of low complexity and impact, may be exempted by the ANM from some of the elements required for the PFM.

With the measures established, the resolution reinforces the tightening of standards related to the protection of health and public safety in mining activities and the need for adequate planning of the closure of mining structures, through monitoring and monitoring of the life of mines and their decommissioning.

[1] According to the definition of Federal Law No. 14,066/2020, which amends the National Dam Safety Policy: "Damage that can occur due to disruption, leakage, infiltration into the ground or malfunction of a dam, regardless of its probability of occurrence, to be graduated according to the loss of human lives and social, economic and environmental impacts."

- Category: Litigation

For years, the matter of how the Public Treasury should behave when becoming aware of the bankruptcy of a legal entity that has a tax enforcement proceeding n(s) against it pending trial was discussed.

Several legal controversies have arisen regarding the possibility of submitting tax credits to the pool of creditors instated by the bankruptcy decree, in accordance with the provisions of Articles 186 and 187 of the National Tax Code (CTN) and article 29 of Law No. 6,830/80 (Tax Enforcement Law). There was also debate about what would be the ideal outcome for the tax enforcement proceeding – termination or suspension – in the event that the Public Treasury chooses to file a proof of claim before the bankruptcy court.

In May 2020, when judging the Special Appeal (REsp) nº 1,857,055 involving the bankrupt airline Vasp, the 3rd Panel of the Superior Court of Justice (STJ) understood that the fact that the Treasury filed the tax enforcement before the decree of bankruptcy would not prevent it from opting for filing a proof of claim within the bankruptcy proceeding. In this decision, it was understood that Article 187 of the CTN does not represent an impediment to the proof of claim, but rather a prerogative of the public entity, who can choose between tax enforcement and bankruptcy proof of claim. However, once opting for the proof of claim, it would be necessary to suspend the tax enforcement.

The 4th Panel of the STJ has a similar understanding, thus consolidating the understanding of the 2nd Section of the STJ on the issue.

The Group of Reserved Chambers of Corporate Law of the Court of Justice of São Paulo, adopting the understanding of the 2nd Section of the STJ, published on January 16, 2020 the Enouncement XI, determining that "the Public Treasury´s option to file a proof of claim to collect its tax credit within bankruptcy proceeding does not require the termination of the tax enforcement proceeding, provided that it proved it has suspended the tax enforcement proceeding in regard to the bankrupt entity". The statement is currently under review, as recently released by the state court.

Although it admitted the possibility of the Public Treasury to file a proof of claim even with the existence of a previous tax enforcement, the 1st Panel of the STJ understood that it would not be necessary to suspend or terminate the tax enforcement proceeding. Both judicial measures could run simultaneously , provided that there was no act of constriction in the tax proceeding. According to that decision, the mere existence of a tax enforcement would not be a guarantee of receipt of the claim due to the public treasury, so that there would be no bis in idem, i.e. the two options would not be being admitted simultaneously.

Little was said about what subjects would be processed and judged by the bankruptcy court, if the Public Treasury decided to file the proof of claim and suspend the tax enforcement proceedings. In other words, would the bankruptcy court have the competence– or even the expertise necessary – to assess matters that would, until then, be assessed by the tax enforcement court, such as the existence, legitimacy and enforceability of the tax credit?

Based on the original wording of Law No. 11,101/2005 (Law of Recovery and Bankruptcy), jurisprudence and doctrine did not address this theme. Marcelo Barbosa Sacramone, however, had an understanding on the subject. For him, if the National Treasury waived the privilege of maintaining its tax enforcement proceeding and chose to file the proof of claim before the bankruptcy court in order to collect its credit in a quicker manner, the bankruptcy court would then become competent to asses and rule on any matter – including the analysis of merit – that involved that credit.[1]

The wording of the new Article 7a of the Recovery and Bankruptcy Law, included by Law No. 14,112/2020, seems to clarify the issue by creating a proper mechanism for tax credits´ proof of claim.

In addition, Paragraph 4, items I and II of Article 7a, delimits which topics related to tax credits would be of the bankruptcy court´s competence, and which would be of the tax enforcement´s competence[2].

In line with the CTN and the Tax Enforcement Law – article 5 of which determines that the competence to asses and rule on the enforcement debt of the Public Treasury registered in the overdue tax debt roster excludes that of any other , including the bankruptcy court – the competence to rule on the existence, if the debt is demandable and the value of credit will be of the tax enforcement court. In other words, the analysis of the merits of the tax enforcement will not be assessed by the bankruptcy court, but by the tax enforcement court.[3]

It is up to the bankruptcy court to rule on topics such as calculation and classification of claims, in addition to those related to the collection of assets, disposial of assets and crditors´payment.[4]

Paragraph 4(V) of Article 7a – in view of the competence of the tax enforcement court to assess the matter mentioned above – states that "tax enforcement proceeding will remain suspended until the bankruptcy is terminated, exception made to the possibility of pursuing co-liable parties."

Despite the changes introduced by Law No. 14,112/2020, which entered into force on January 23, 2021, the 1st Section of the STJ, in May of this year, unanimously referred to trial under the rite of repetitive appeals REsp 1.891.836/SP, theme 1,092, with the following thesis at issue: "Possibility of the Public Treasury filing a proof of claim regarding a tax credit which is subject to an ongoing tax enforcement proceeding".[5]

Although the National Treasury has suggested that the thesis should not be made in relation to proof of claims made after Law No. 14,112/2020 came into force – considering that it expressly included the possibility of filing a proof of claim even if there is already an ongoing tax enforcement proceeding –, Minister Gurgel de Faria (rapporteur for the appeal) considered that this issue should be dealt with when the merits of the legal question are examined. Thus, currently, the outcome of the subject is awaited.

[1] "If you waive this privilege and file the proof of claim before the bankruptcy court, the bankruptcy court becomes competent for the assessment of all matters involving that claim. The justification is that the privileged treatment of the tax credit is guaranteed so that it continues with tax enforcement, so that only that judgment can assess the various issues involving that claim, such as prior payment, the absence of the obligation or possible compensation.

However, in order to accelerate its satisfaction, the Treasury could waive the privilege of maintaining its tax enforcement proceeding and choose to file the proof of claim before the bankruptcy court . With the waiver, it would allow all questions to be assessed by the bankruptcy court itself, so that it can define whether and by what amount the credit should be enforced. What cannot occur, however, is the bis in idem, i.e. having your credit paid by two different choices. The proof claim, if submitted after the filing of the tax enforcement, must be terminated, for lack of interest to act. This is because there can be no overlap of forms of satisfaction."

SACRAMONE, Marcelo Barbosa (Comments to the Business Recovery and Bankruptcy Act. São Paulo: Saraiva, 2018, p. 83.

[2] It is necessary to clarify that there are still no judgments facing this issue, due to the fact that Law No. 14,112/2020 is recent and has entered into force only at the end of January 2021.

[3] SACRAMONE, Marcelo Barbosa. Comments to the Business Recovery and Bankruptcy Act. São Paulo: Saraiva, 2021, p. 121.

[4] The issue of the constriction of assets was also the subject of Theme 987 of the STJ - "Possibility of the practice of constrictive acts, in the face of a company in judicial recovery, in the case of tax enforcemente of tax and non-tax debt" – which, however, lost its object due to the new provisions of the Recovery and Bankruptcy Law brought by Law No. 14,112/2020.

[5] Also, unanimously, it was decided to suspend special appeals at second instance and/or in the Superior Court related to this subject.

- Category: Competition

In recent trial sessions, the Court of the Administrative Council of Economic Defense (Cade) discussed whether the non-establishment of administrative proceedings to investigate alleged anticompetitive crimes reported by the signatories of leniency agreements would prevent them to obtain the certification of proper execution. Leniency Agreements are an important instrument for Cade'senforcement, especially for the investigation of collusive practices that are difficult to detect, such as cartels.

Cade’s General Superintendence (“CADE/SG”)is the body responsible for signing the Leniency Agreements, while the Cade Court is responsible for verifying if the agreement was executed in accordance with its terms. Once the Court certifies that the agreements were properly executed, it confirms the benefits sought by the signatories: the termination of Cade's punitive action or the reduction of applicable administrative penalties, as well as the extinction of the punishability of crimes related to cartel practice.

In the case examined, which runs under secrecy, the rapporteur councillor considered that the Leniency Agreement could not be certified as executed, sinceits content was not able to assist in the investigation of the reported anticompetitiveacts. In his opinion, the opening of an administrative proceeding to investigate the unlawful acts reported would be a consequence of the contributions made by the signatories during the investigation phase conducted by Cade’sGeneral Superintendence.

The rapporteur explained that the evidence brought by the signatories was uncompelling and that there were others that could have generated a different outcome from the filing of the administrative inquiry based on the information provided by the signatories. The rapporteur did not discriminate such evidence because of the secrecy of the procedure, but he mentionned,as an example, ongoing procedures in the Federal Prosecutor's Office that could have been presented by the signatories.

Accordingly, the rapporteur voted against the certification of the execution of the Leniency Agreement, on the gorunds that the signatories did not produce sufficient evidence for the administrative inquiry to result in the openingof an administrative proceeding able to investigate and punish alleged anticompetitive acts.

Another counselor of the Cade Court disagreed, understanding that, in fact, it would be up to the General Superintendence to evaluate the evidence offered when signingthe leniency agreement and to conduct investigations based on the information brought by the signatories.

According to the counselor, the signatory is not aware of the entire evidential set of which the General Superintendence has at the time of the signingof the agreement, so that it cannot foresee the repercussions of the evidence brought by him or her in the investigations promoted by the General Superintendence. Other members of the Cade Court stressed that it is up to the General Superintendence to establish minimum standards of proof for the signingof leniency agreements, and it also hasthe prerogative to examine such evidence, not the Cade Court.

In view of this discussion, the plenary, by a majority, certified that the leniency agreement was properly executedAlso, the Court established that the upcoming decision of the General Superintendence not to open an administrative proceeding would not be a reasonnot to certify its execution.

The plenary decision highlighted Cade's concern not to transfer the burden of the investigation’s results to the signatories of the Leniency Agreement, who would have fullfiledall the obligations under which they commited themselves to deliver all documents and information available to them about the facts reported.

- Category: Tax

As a result of Law No. 13,988/20, which regulates the tax transaction provided for in the National Tax Code (art. 171)[1], the Federal Revenue Service of Brazil (RFB) and the Attorney General's Office of the National Treasury (PGFN) signed, on April 18, 2021, notice of a new modality of transaction by membership, which involves social security contributions and to other entities and funds on profit sharing (PLR), in breach of Law No. 10,101/00.

Although tax transactions are already foreseen and regulated for situations which, in accordance with the definition contained in the legislation, involve unrecoverable and difficult claims, this is the first time that the Union has elected a specific litigious thesis to enter into a transaction with the taxpayer, regardless of the possibility of recovery of the claim.

The new transaction modality will have as scope administrative or judicial processes that deal specifically with:

- PLR-Employees: interpretation of the legal requirements for the payment of PLR to employees without the incidence of social security contributions and

- PLR-Directors: legal possibility of payment of PLR to directors not employed without the incidence of social security contributions.

According to information available so far, the taxpayer who opts for the new mode of transaction shall indicate all tax debts that see the legal controversy in reference, in addition to irrevocably and irrevocably confessing to be debtor of said debts, giving up the respective administrative and judicial discussions and renouncing the claims of law on which they are founded.

It is important to emphasize that those who adhere to the new modality should be subject to the understanding given by the Tax Authorities to the legal controversy transuded, including in relation to future or unconsummated generating facts, a measure that aims to end discussions on the subject.

The agreement may be formalized between July 1 and August 31, 2021. The procedures and resources of this transaction will be centralized in the e-CAC system (cav.receita.fazenda.gov.br), if the debt is linked to RFB, and on the Regularize portal (www.regularize.pgfn.gov.br), if the debit is linked to the PGFN. The taxpayer must give consent to the sending of communications to the tax domicile.

Payment can be made within five years, applying the Selic fee. The discounts granted will be applied in a regressive manner, focusing on principal, fine, interest and charges, depending on the number of installments paid. Initially, it is necessary to pay 5% of the tax debt without reductions, which can be divided into up to five successive monthly installments. The applicable discounts are indicated in the table below:

| Installment | Initial installments (no discount) | Number of additional parcels | Discount percentage |

|

Up to 1 year

|

5% of the total value in 5 installments | 1 to 7 | 50% |

| Up to 3 years | 8 to 31 | 40% | |

| Up to 5 years | 32 to 55 | 30% |

The processes with judicial deposit require special attention, because, according to the notice, the agreement to the transaction will imply the automatic conversion of deposits into union income, and the above payment terms will be applied only to the remaining balance of the debt.

It is also noteworthy that the adhering to the tax transaction does not imply the release of the taxes resulting from the bearing of assets, fiscal injunctive relief and the guarantees provided administratively, in the actions of tax execution or in any other legal action. Such exemption will occur only after the discharge of the tax debt.

The notice also brings the obligations to be assumed by the adherent, which involve transparency about their economic situation, maintenance of fiscal regularity and before the FGTS, maintenance of solvency before the Tax Authorities, among others.

Considering that this is a legal thesis Contested and which involves significant amounts, there is expectation in relation to the evolution of the theme to reduce litigation.

[1] Art. 171. The law may provide, under the conditions it establishes, to the active and passive persons of the tax obligation to enter into a transaction that, through mutual concessions, imports in dispute determination and consequent extinction of tax credit.

Single paragraph. The law shall appoint the competent authority to authorize the transaction in each case.

- Category: Real estate

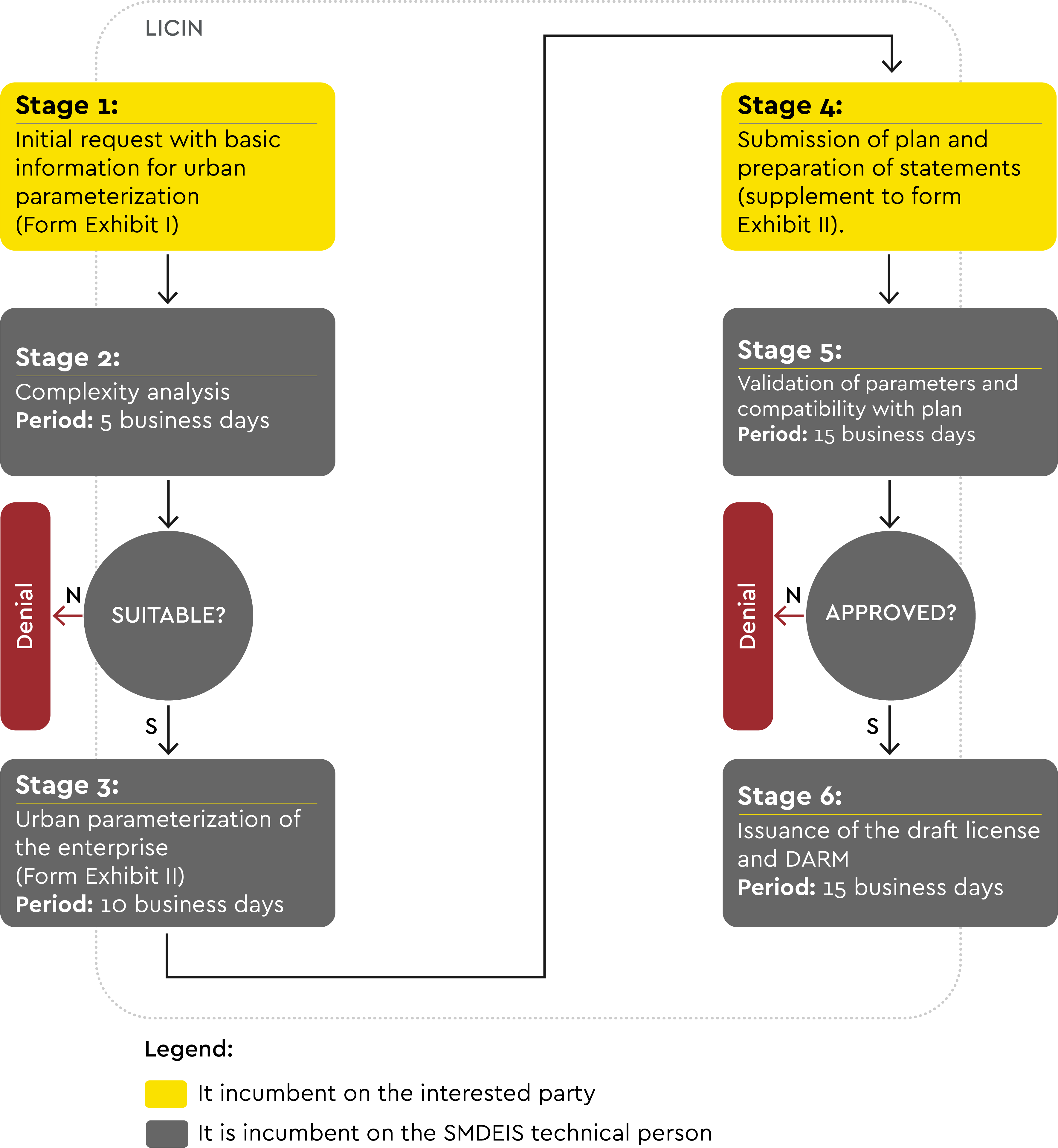

As part of the #InvistaNoRio campaign, an initiative of the Municipal Bureau for Economic Development, Innovation and Simplification (SMDEIS) to boost business in the city of Rio de Janeiro, Municipal Decree No. 48,719/21 was published on April 6, which provides for the Integrated Building Licensing (Licin) procedure and aims to cut the red tape for applications for urban permits for new construction in the city.

The procedure previously took up to one year, but since April it has been possible to obtain project approval within 30 business days (excluding the deadline for issuing the license by the bureau after approval). The initiative promises to attract more investments for the city in the construction sector and the real estate market, since the delay in licensing was one of the main obstacles for companies in the business operating in the city.

The objective was to unify and simplify the stages of the licensing process in the city. Most of the information needed for the project, for example, was self-declared by the professionals responsible for architectural design (PRPA) and the execution of the works (PREO). According to the standard published, full compliance with the parameters and requirements of the Rio de Janeiro Master Plan, the Land Parceling, Use and Occupation Legislation, the Municipal Simplified Works, and Buildings Code and other urban planning legislation and technical standards in force at the municipal, state, and federal levels was also under the responsibility of the same professionals, together with the interested parties.

From now on, the procedures for approving architectural plans should observe the following steps:

- Submission of the initial application by the applicant, by means of a form accompanied by the documentation provided for in the legislation;

- Evaluation of the information declared by the interested partyto identify non-conformities and classification in Licin;

- Filling out a new form by SMDEIS technical personnel, with an indication of the parameters required by the legislation;

- Supplementation of the form by the responsible professionals and the interested party, with an application for approval of architectural plan, accompanied by presentation of the plan;

- Approval and validation of the fulfillment of the planned parameters and their compatibility with the plan presented by SMDEIS technical personnel; and

- Issuance of the license draft and form for payment of the municipal fee through DARM.

As the diagram below shows, the steps described in the items 2, 3, 5 and 6 are the responsibility of qualified SMDEIS technical personnel and shall be carried out within the deadlines illustrated below. The fulfillment of requests and requirements must be done by interested parties within 30 business days, under penalty of cancelation.

All plans that were already in progress may migrate to the Licin procedure, provided that the steps described above are covered. This migration must be done at the request of the applicant in writing.

As an exception, plans for buildings of great complexity are not subject to the above deadlines, as well as those involving buildings or groups with more than 500 units, buildings protected by heritage protection, which depend on the payment of consideration or grants tied with obligations, among other criteria[1] defined in SMDEIS Resolution No. 10, of February 1, 2021.

In such cases, the plan should be submitted at the opening of the process due to the need for a specific analysis. However, after the necessary authorizations and/or consents from the responsible agencies have been obtained, the plans of buildings of great complexity will be able to follow the same steps provided for other constructions. Documents proving authorizations must be submitted together with the data and information provided in the first stage of the Licin process.

Article 5 of Municipal Decree No. 48,719/21 also provides that the construction license via Licin will be issued upon presentation of the protocol number formalized in the agencies whose response is required for licensing. Its validity will be conditional on the assent of such agencies. Once all the requirements are met, the license must be issued, setting the maximum period of three months for the presentation of the agreement of all agencies, which may be extended until the works begin, according to the declaration regarding the phase of the work. The works may not begin until the cancellations are obtained by the applicant.

Once the building permit is obtained, the interested party will be responsible for reporting in the administrative process of the Licin procedure the dates of commencement of the works, completion of foundations, the first slab, and, finally, the works, when inspection will be carried out for the purposes of issuing a certificate of acceptance of works (commonly called Habite-se).

Given that the new decree came into force on the date of its publication on April 6, construction companies and the real estate market should already comply with the new rules for future ventures and may migrate the ongoing licensing processes to the Licin procedure.

Although the speed of the processes depends on the actions of the other bodies not subordinate to the City of Rio de Janeiro, the expectation is that the approvals for architectural plans with application of the Licin procedure will facilitate the performance of the real estate business in the city of Rio de Janeiro.

[1] Plans of great complexity are considered to be: (a) groups of buildings with more than 500 units, including integrated groups; (b) lots included in more than one urban zoning and/or subject to bands of influence with parameters different from those applied in the remainder of the lot; (c) lots that are in locations devoid of urban infrastructure and requiring execution of an urbanization consent; (d) land parceling projects; (e) projects involving assets that are subject to heritage protection or preserved projects in any sphere; (f) projects involving processing of investiture; (g) sites where the application of projected alignments (PAA) generates inconsistency in analysis; (h) projects that require specific environmental analysis, such as: (h.1) located on the beachfront; (h.2) found within or bordering environmental conservation units, except APA; (h.3) imply removal of plant cover subject to authorization and/or management of wild fauna; (h.4) depending on prior use, point to possible contamination of the land; and (h.5) intervention in areas of permanent preservation, as defined by Federal Law No. 12,651, of May 25, 2012; and (i) projects that depend on payment of consideration or a grant imposing an obligation for licensing.

- Category: Banking, insurance and finance

Bruno Racy, Roberto Kerr Cavalcante Bonometti and Frederico Antelo

The agribusiness sector and financing alternatives for the agribusiness chain have been the subject of important changes and improvements in the last year. The conversion of Executive Order No. 897/19 (the Agro MP) into Law No. 13,986/20 brought about various innovations aimed at stimulating access to credit, especially through capital market funding. Among them, the following stand out:

- the establishment of the Solidarity Guarantee Fund;

- the creation of collateralized rural assets;

- the institution of the Rural Real Estate Note (CIR);

- the expansion of the parties authorized to issue Rural Product Notes (CPR) to include rural producers (whether individuals or legal entities), cooperatives, and associations of producers that act in the production, marketing, and industrialization of rural products, as well as the possibility of indexing the security to exchange rate variation; and

- the possibility of creating and executing real guarantees on rural properties, including through payment in kind or otherwise.

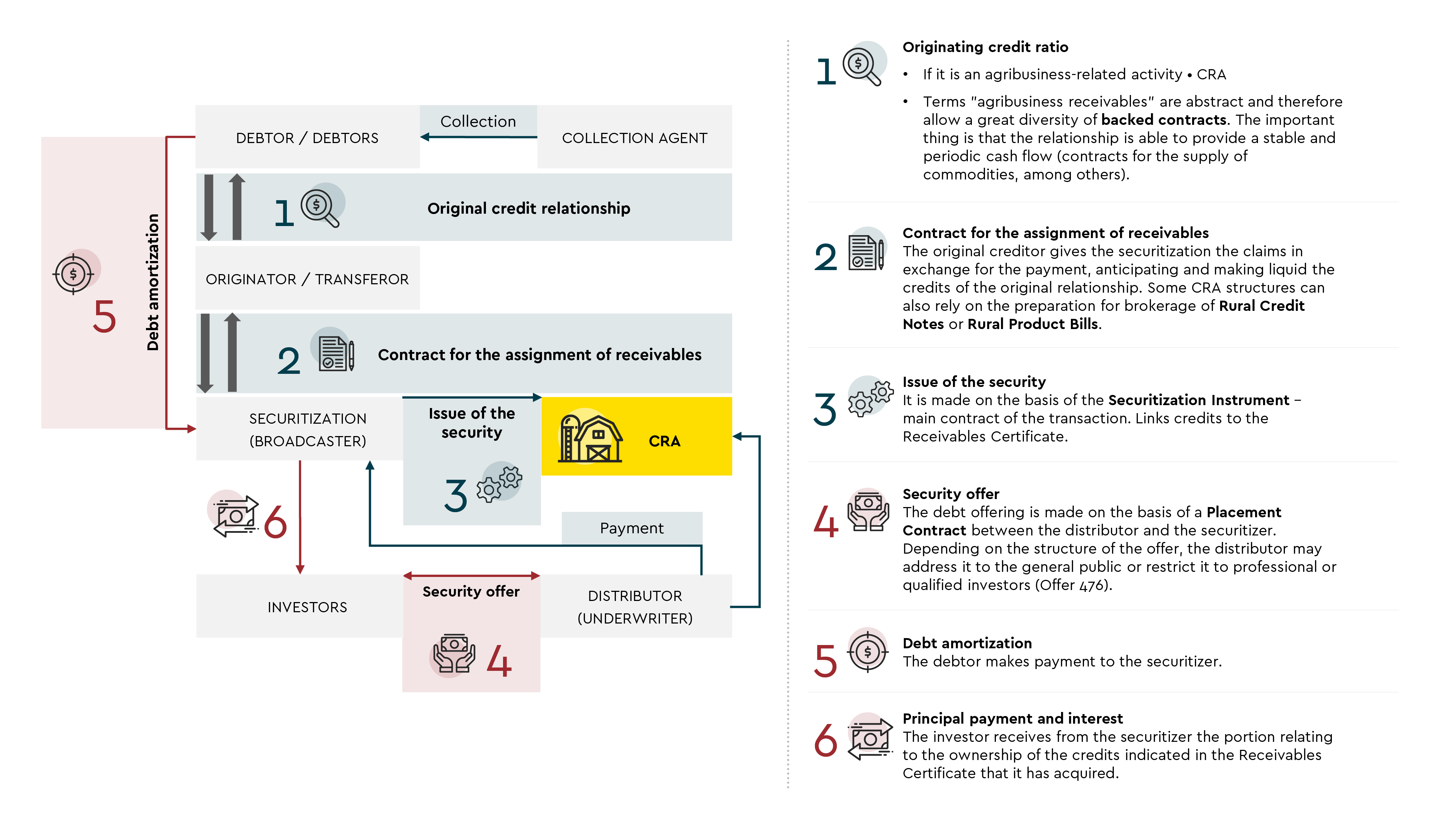

These advances have had a strong effect on the Agribusiness Receivables Certificate (CRA) market, which has been very heated in the last year. According to Anbima data (Brazilian Association of Financial and Capital Markets Entities), in 2020, 586 issuances were conducted for public distribution of CRA, totaling approximately R$ 95.8 billion. This corresponds to a 31% increase in the volume of issuances and a 21% increase in the number compared to 2019.

CRAs are fixed income securities issued by a securitizer and backed by receivables originating from business between farmers, or their cooperatives, and third parties. These businesses include financing or loans related to the production, marketing, processing, or industrialization of products, agricultural supplies, or machinery and implements used in agricultural production, as provided for in Article 23, paragraph 1 of Law No. 11,076/04.

The diagram below summarizes the structure of a CRA issuance:

Article 3, paragraph 4, of CVM Instruction No. 600 establishes that receivables rights may be considered to back (or securitize) an offer of CRA when created: (i) directly by debtors or original creditors characterized as rural producers or their cooperatives, regardless of the destination to be given by the debtor or the transferor to the funds; or (ii) debt securities issued by third parties linked to a commercial relationship between the third party and rural producers or their cooperatives; or (iii) debt securities issued by farmers or their cooperatives. This provision of CVM Instruction No. 600 reflects various CVM precedents regarding Law No. 11,076/04, through which the interpretation of credits that may contain CRA offers, including those that are at the end of the agribusiness production chain, has been expanded.

In addition to the nature indicated above, these receivables rights can be used in various ways, such as trade acceptance bills, Rural Product Notes (CPR), Promissory Notes (NP), Agribusiness Credit Rights Certificates (CDCA), debentures, Export Credit Notes (NCE), Export Credit Bills (CCE), Supply Contracts or Rural Real Estate Notes (CIR).

The CRAs market tends to become even more attractive to investors after the creation of CRA Garantido [Collateralized CRA] on April 8. It is a new product through which the National Bank for Economic and Social Development (BNDES) will act as a guarantor for investors in a CRA issuance.

The operation that inaugurated this product was the issuance of CRA from Ecoagro – a securitization firm specialized in agribusiness – based on receivables rights of Cotrijal Cooperativa Agropecuária e Industrial, with 7,700 more cooperative members.

In the case of the issuance announced, BNDES guaranteed only the CRAs of the first series (through an endorsement of the bank), which will be considered senior in relation to the CRAs of the other series, so that they will have priority (a) in receiving the remuneration; (b) in payments arising from extraordinary amortization and/or early redemption, as the case may be; (c) in the payment of the unit par value; and (d) in the event of separate equity settlement.

In the event of late payment, non-compliance with obligations, and/or if it is necessary to re-compute the escrow accounts in which the agribusiness receivables rights that backed the issuance are deposited, the fiduciary agent (as a representative of the holders of the CRAs of the first series) or the issuer may notify BNDES to make payment of the principal and interest due.

Bndes' intention with this new product is to guarantee the payment of the securities to investors and, with this, to promote access to the capital markets by small and medium-sized rural producers. With the unprecedented participation of BNDES as guarantor in the scope of CRA offers, the expectation is that this measure will result in:

- reduction in the financial costs of operations for rural producers and/or their cooperatives, since the guarantee given by BNDES mitigates the risk of default and, consequently, allows allocation of lower interest to the securities;

- greater security for those who invest in CRAs and, consequently, more interest in these securities, since, unlike LCAs (another fixed income instrument used to regulate exposure to the agribusiness sector), CRAs are not guaranteed by the Credit Guarantee Fund;

- complementing the alternative sources of financing for rural producers, or cooperatives, with more incentive to raise money in the capital market outside the traditional financial system; and

- stricter compliance with social and environmental standards, since it is a fundamental requirement for BNDES’

In line with the growing support of investors and funders for ESG analyses, another strategy to further increase the attractiveness of CRAs is the possibility of obtaining environmental and social certifications, such as green bonds or social bonds. In such cases, CRAs undergo a certification process by entities such as the Climate Bonds Initiative (CBI), which establish the criteria for issuing these certifications. By attracting investors who would not initially be interested and increasing demand for such securities, these certifications may also lead to reduced financial costs for the operation.

The constant growth of agribusiness, driven, among other factors, by the various forms of stimulus given to the sector, and now added to BNDES' performance as guarantor and the possibility of certification of CRAs as green bonds, makes the option of financing through these securities an increasingly interesting alternative for rural producers, as such structures tend to attract more investors.