Publications

- Category: Environmental

If viewed as a country, the international civil aviation sector would have the world's 20th GDP but would be among the top ten polluters, with over 2% of global greenhouse gas emissions. It is a significant and rapidly growing environmental impact, with consequences not only for accelerating climate change, but also for the image of the sector in the public eye.

Concerned with changing this scenario, civil aviation companies have been moving to propose measures that contribute to the achievement of the goals set out in the Paris Agreement, a global climate treaty signed during the 2015 United Nations Climate Change Conference (COP 21).

Approved by the 195 nations that are part of the United Nations Framework Convention on Climate Change (UNFCCC), the agreement contains measures for “holding the increase in the global average temperature to well below 2°C above pre-industrial levels,” a limit pointed to as safe by the Intergovernmental Panel on Climate Change (IPCC) to avoid much of the unwanted consequences of global warming.

The agreement only entered into force in November of 2016, after ratification by at least 55 countries responsible for 55% of global greenhouse gas (GHG) emissions. Brazil concluded its ratification process on September 12 of the same year.

In addition to establishing national commitments, the Paris Agreement has also triggered a number of movements among private companies. In the civil aviation sector, Icao (International Civil Aviation Organization), represented by 191 countries, launched the first global agreement to reduce emissions in this segment. In October of 2016, the entity approved the “Carbon Offsetting and Reduction Scheme for International Aviation” (Corsia) through Resolution A 39-3.

The resolution clarifies that in order to achieve the goals of reducing greenhouse gas emissions, a “basket of mitigation measures” was adopted, which includes:

- development of technologies and new standards for aircraft;

- improved air traffic control and ground operations for fuel economy; and

- use of biofuels.

Given the growth in international air traffic, however, Icao recognizes that the measures detailed above are not sufficient to achieve the desired reduction in CO2 emissions. To do so, it is necessary to implement emissions trading and offset mechanisms, just as Corsia also provides, by purchasing carbon credits generated by other sectors and initiatives.

The scheme was structured in three phases, having as a reference (or baseline) the projection of emissions for 2020. From this level, any increase in emissions found must be offset.

The first two phases will be voluntary participation by countries and companies: a “pilot” phase between 2021 and 2023, followed by an “initial” phase between 2024 and 2026. From 2027 to 2035, “Emission reduction measures and targets will apply to all countries except least developed countries, small developing islands, and countries that do not meet a minimum percentage of contribution to total emissions of the sector.”

Study of the Institute for Conservation and Development of the Amazon (Idesam) states that “by July of 2018, 72 countries had committed to voluntarily participating in Corsia from its pilot phase, which represents 70% of international aviation-related activities. Brazil has not yet acceded to the agreement and has pledged to participate only in the mandatory phase starting in 2027.”

Under the rules of the mechanism, the countries of origin and destination of the flight must accede to the agreement for the obligation to reduce and offset emissions from the flight between the two countries to apply at either stage of the scheme. If Brazil does not participate in the voluntary phases between 2021 and 2026, airlines from other countries are exempt from offsetting their emissions in travel to Brazil during this period, which tends to attract foreign competition to Brazil.

Offsetting is an old instrument that began to be used with the approval of the Kyoto Protocol in 1997 and now has a new incentive to be employed on a large scale through Corsia.

This mechanism is basically through the purchase of certified carbon credits, which may be issued by different project types, such as:

- forest projects, involving replanting forests or measures to prevent deforestation;

- energy projects, which may be related to renewable sources of energy or energy efficiency; and

- exchange of non-renewable and high-emission greenhouse gas fuels for renewable fuels.

The voluntary accession of Brazil and Brazilian companies to Corsia will undoubtedly produce environmental benefits by sponsoring carbon credit generating projects and contributing to the central objective of the Paris Agreement, which is to curb global warming.

It is a movement that can have a positive impact on the image of these companies, considering that most passengers on international flights care about global warming and would even be willing to pay more for an airline ticket in order to offset the emissions from the flight.

One of the most attractive incentives for Brazilian companies to voluntarily join Corsia, however, would be the increased competitiveness that the measure can provide, as it forces foreign companies to do the same, incurring costs many times higher than domestic ones.

- Category: Banking, insurance and finance

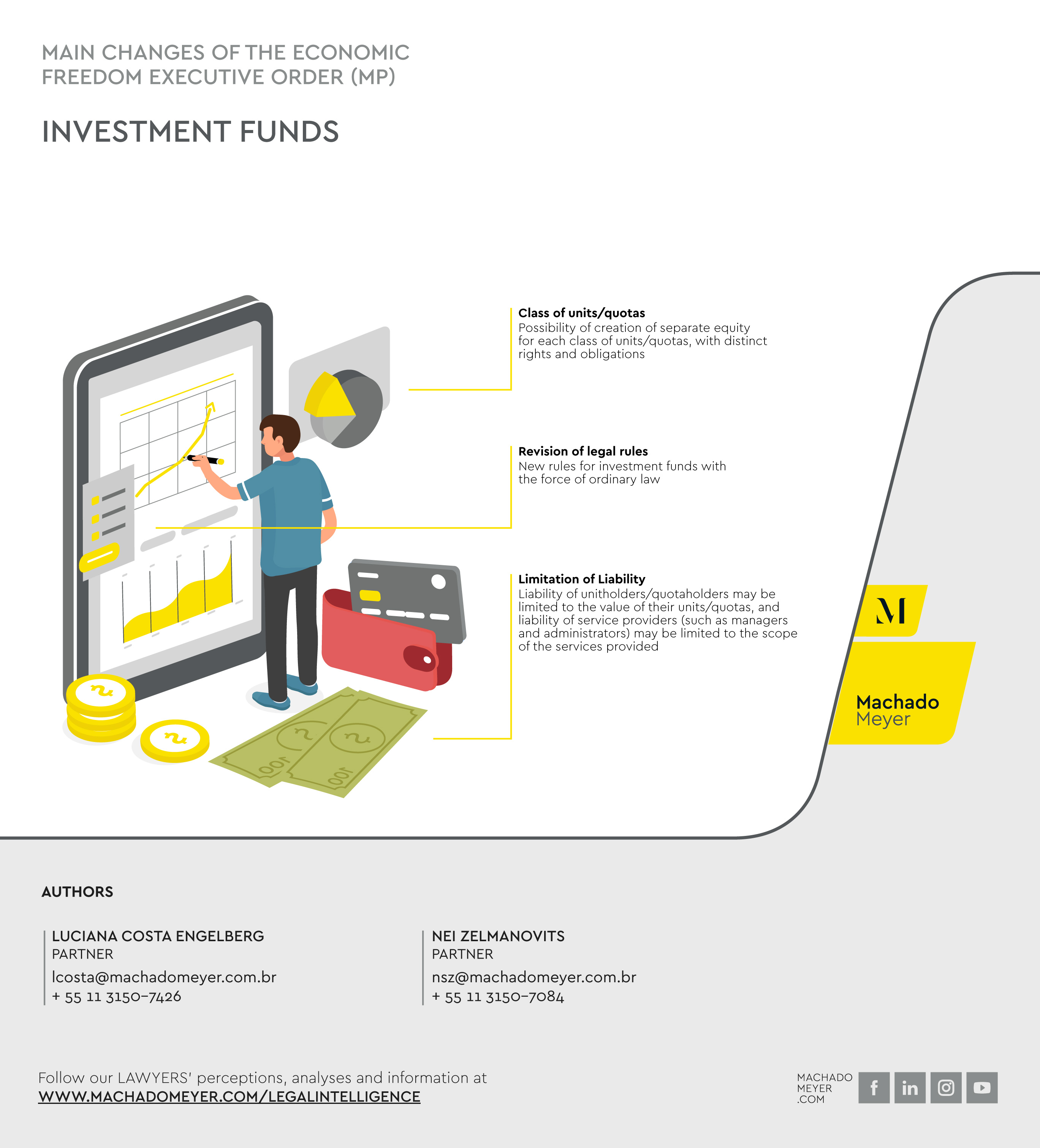

Investment Funds

On September 20, 2019, Federal Law No. 13,874/19 was enacted, setting forth the Declaration of Rights of Economic Freedom. Among the changes promoted by the new law, we highlight innovations for the investment fund industry, with the introduction of a new chapter in the Brazilian Civil Code on the subject (articles 1,368-C to 1,368-F).

The law defined investment funds as a condominium of a special nature, intended for investment in financial assets, property, and rights of any nature, having expressly excluded the application to investment funds of the rules related to condominiums in general provided for in articles 1,314 to 1,358-A of the Civil Code, an understanding that had been adopted by the industry until recently.

The removal of the application of the rules dealing with condominiums in general is in line with the changes brought about by the law regarding the possibility of limitation of the liability of investment fund unitholders. This is so because, according to the interpretation of the general rules on condominiums (and applied to investment funds), unitholders should have unlimited liability for the obligations undertaken by the investment fund (which does not have corporate existence). In that respect, article 15 of CVM Instruction No. 555, of December 17, 2014 (“CVM Instruction 555”), provides that unitholders are liable for any negative equity of the fund.

In addition, Law No. 13,874/19 confirmed the jurisdiction of the Brazilian Securities and Exchange Commission (CVM) to regulate investment funds defined by law and the changes brought in by the new law.

Below we highlight the main aspects of Law No. 13,874/19 dealing with investment funds.

Recording

Pursuant to the third paragraph of the new article 1,368-C of the Civil Code, the recording of investment funds’ bylaws with the CVM is a condition sufficient to ensure their publicity and effectiveness vis-à-vis third parties.

With this change, it will no longer be necessary to record the bylaws of investment funds with a register of deeds and documents, as was previously provided for in CVM regulations.

This was the first issue to be regulated by CVM since the promulgation of Law No. 13,874/19. On October 2, 2019, CVM issued CVM Instruction No. 615, which amends several Instructions issued by the CVM, so as to revoke the requirement of a certificate of recording of an investment fund’s bylaws with the register of deeds and documents.

The change meets the demands of the industry for reducing paperwork and costs.

Limitation of liability of unitholders and unit classes

In line with protecting investors and limiting their liability with respect to the obligations of the investment fund, Law No. 13,874/19 innovated by providing that a fund's bylaws may provide for a limitation on the liability of investors to the value of their units, thereby protecting investors from being liable for obligations of the fund that exceed their holding in the fund.

Also, the bylaws may establish unit classes with distinct rights and obligations, with the possibility of setting up segregated equity for each class, and such segregated equity will only be liable for obligations linked to the respective class, under the terms of the bylaws.

Please note that the adoption of the principle of limited liability by an investment fund originally formed without a limitation is possible but in this case the limitation will only cover events taking place after the respective change in its bylaws. That is, until the matter is regulated by the CVM and the fund's bylaws are amended so as to include a limitation of liability, unitholders will be liable, in proportion to their holding, for the fund's obligations regarding facts that occurred prior to the amendment of the bylaws.

Currently, CVM regulations applicable to private equity investment funds (CVM Instruction 578 of August 30, 2016) allow, in certain situations, for the fund's bylaws to assign to one or more classes of units different economic and financial rights. As a general rule, the different economic rights of the unit classes are limited to the fixing of administration and management fees and order of preference in the payment of income, amortization, or liquidation balance of the fund. In turn, for funds intended exclusively for professional investors[1] or those receiving direct financial support from funding organizations, it is permitted to assign one or more different classes of units economic rights different from those provided for above.

Until the enactment of Law No. 13,874/19, however, there was no specific provision regarding the possibility of setting up segregated equity for each class of unit and limitation of liability of the unitholder for the obligations linked to the respective class. This is one of the major advances the new law brings to the fund industry, which not only allows for cost savings (often via the choice of new fund structures for each investment strategy), but also greater legal certainty for to investors.

It is worth noting that the limitation of unitholder liability and segregation of fund assets by different unit classes are still subject to CVM regulations.

Bankruptcy System

Also in the context of the unitholders' limitation of liability, Law No. 13,874/19 provides that investment funds are directly liable for the legal and contractual obligations assumed by them, and if the limited liability fund does not have sufficient equity to settle its debts, the insolvency rules contained in articles 955 to 965 of the Civil Code shall apply.

Insolvency may be requested in court by creditors, per a resolution by the investment fund's unitholders, pursuant to its bylaws, or by the CVM itself.

The new article 1,368-E of the Civil Code also provides that service providers of the investment fund are not liable for the fund's obligations (except for the losses they cause when they act under willful misconduct or bad faith).

Thus, any liability of the fund could not directly affect the equity of the unitholders, nor the service providers of the fund, as it is mandatory to follow the bankruptcy process for the fund if it does not have sufficient equity to settle its debts.

The table below summarizes the main aspects of the bankruptcy system provided for in the Civil Code:

|

Rules of the bankruptcy system |

|

|

Declaration of Bankruptcy |

Bankruptcy is declared whenever debts exceed the amount of the debtor's assets. |

|

Preferences |

ü If there is no legal title to preference, creditors shall have equal rights over the assets of the common debtor. ü Legal titles to preferences are in rem privileges and rights. ü In rem claims have preference over in personam of any kind; in personam claims have preference over simple claims; and special privileges are over general ones. ü When two or more creditors of the same specially privileged class compete for the same assets, and with like title, there shall be a pro rata apportionment among them in proportion to the value of the respective claims, if the result is not sufficient for the full payment of all of them. ü The special privilege includes only the assets subject, by express provision of law, to the payment of the claim which it favors; and the general privilege includes all assets not subject to in rem claim or special privilege. |

The application of the new bankruptcy rules to investment funds is also subject to regulations in due time by the CVM.

Liability of service providers

In addition to limiting the liability of unitholders, Law No. 13,874/19 contemplates the possibility of limiting the liability of investment fund service providers to the fulfillment of their particular duties, without joint and several liability.

Currently, CVM Instruction 555 and CVM Instruction 578 provide for joint and several liability between the fund manager and third parties hired by the fund for any losses caused to unitholders as a result of conduct contrary to law, regulation, or normative acts issued by the CVM. The regulations applicable to receivables investment funds (FIDC) and real estate investment funds (FII), on the other hand, have no such provision, such that for FIDCs and FIIs it would already be possible to apply the limitation of liability provided for in Law No. 13,874/19.

Conclusions

The changes brought about by Law No. 13,874/19 are an important milestone in the evolution of the fund industry in Brazil, aiming at reducing bureaucracy, costs, and greater investor security, bringing the industry closer to practices adopted in other jurisdictions.

However, changes to the new law are still subject to CVM regulations for their effective application. In this context, the CVM will submit for public hearing an instruction to amend the current regulations in accordance with the provisions of the new law.

[1] Per the terms of article 9-A of CVM Instruction Instruction No. 539, of November 13, 2013, the following are considered professional investors:

I - financial institutions and other institutions authorized to operate by the Central Bank of Brazil;

II - insurance companies and capitalization companies;

III - open-ended and closed-ended supplementary private pension entities;

IV - individuals or legal entities who have financial investments in the amount of more than ten million Brazilian Reais (R$ 10,000,000.00) and, in addition, attest in writing to their status as a professional investor through a separate instrument, in accordance with Exhibit 9-A;

V - investment funds;

VI - investment clubs, provided they have a portfolio managed by a securities portfolio manager authorized by the CVM;

VII - independent investment agents, portfolio managers, analysts, and securities consultants authorized by the CVM, in relation to their own funds;

VIII - non-resident investors.

- Category: Litigation

When property owners decide to file an eviction action against tenants, all means of repossessing the property have generally been exhausted. This indicates the urgency that lessors have in obtaining a preliminary court order that the property be returned.

However, this judicial relief may sometimes take longer than expected, frustrating property owners' expectations and possibly exposing them to irreparable damage, especially where the lease does not have one of the forms of guarantee (security deposit, surety, surety insurance, for example) set forth in Article 37 of the Lease Law (Law No. 8,245/91).

In view of this situation, the Lease Law, amended mainly by Laws 12,112/09 and 12,744/12, now allows property owners to obtain injunctions for eviction of properties within 15 days, regardless of the tenant's response in the proceeding and provided that a deposit equivalent to three months' rent is made. This prerogative applies to eviction actions that are based solely on non-payment of lease payments and ancillary fees, in lease agreements without any guarantees, pursuant to Article 59, item IX, of the Lease Law.

Although, at first, the case law did not take an incisive position as to the applicability of this legal provision, the Judiciary seemed to have understood the spirit of innovation intended by the Lease Law, aiming at noticeable evolution of the topic over time.

Upon reviewing the case law of the São Paulo State Court of Appeals (TJ-SP), for example, one notes that many judicial decisions use this legal provision as grounds for granting an injunction sought by the lessor and order eviction from the property by lessee within 15 days.[1] The Rio de Janeiro State Court of Appeals (TJ-RJ) has been following the same understanding.[2]

In only one of several judgments on the matter in recent years, the TJ-SP acknowledged that the requirements set forth in Article 59, item IX, of the Lease Law were met, but upheld the lower court’s decision that had dismissed the injunction for eviction in 15 days, arguing that “given the specific situation, the granting of the injunction for eviction would be premature, without enabling the hearing/defense of the opposing party” (Interlocutory Appeal No. 2078843-81.2019.8.26.0000, 32nd Chamber of Private Law, decided on April 25, 2019).

That is, the prevailing position in the case law is that, given the authorizing legal requirements, the injunction provided for in Article 59, item IX, of the Lease Law must be granted and the property must be vacated by the lessee within 15 days. In other words, the case law has evolved over time to reflect the change in the Lease Law and to ensure its application and the effectiveness of its provisions. In this respect, it provides less protection to the tenants and is more directed to addressing the rights and interests of lessors harmed by default in lease payments that do not have the provision of guarantees in their favor.

Thus, it is possible to state that the advance in the case law regarding effective application of the provisions of Article 59, item IX, of the Lease Law is positive for lessors and generates a greater supply of properties for lease, resulting in an impact on average market prices. Indirectly, therefore, it also benefits tenants, as property owners are more secure in renting them out to those who are unable to provide a guarantee at the time of the lease agreement, or in maintaining the deal already entered into if the guarantee comes to be terminated during the term of the contract.

[1] TJ-SP: Interlocutory Appeal No. 2273636-54.2018.8.26.0000, 25th Chamber of Private Law, decided on May 28, 2019; Interlocutory Appeal No. 2064553-61.2019.8.26.0000, 32nd Chamber of Private Law, decided on May 10, 2019; Interlocutory Appeal No. 2053445-35.2019.8.26.0000, 31st Chamber of Private Law, decided on July 25, 2017; and Interlocutory Appeal No. 2267446-75.2018.8.26.0000, 32nd Chamber of Private Law, decided on April 11, 2013.

[2] TJ-RJ, Interlocutory Appeal No. 0026990-62.2019.8.19.0000, 22nd Civil Chamber, decided on September 10, 2019; Interlocutory Appeal No. 0051387-88.2019.8.19.0000, 6th Civil Chamber, decided on June 28, 2019; Interlocutory Appeal No. 0067138-52.2018.8.19.0000, 15th Civil Chamber, decided on May 21, 2019, and Interlocutory Appeal No. 0023138-30.2019.8.19.0000, 19th Civil Chamber, decided on August 6, 2019.

- Category: Competition

The Administrative Council for Economic Defense (Cade) has reviewed about 40 merger filings involving the so called associative agreements since Resolution No. 17/2016 entered into force on November 25, 2016. These filings refer to agreements between companies from the most varied of industries (such as food and beverage, cement, pharmaceuticals, shipping, and telecommunications) and with different subject matter (distribution, supply, infrastructure operation, commercial partnerships, co-development, and joint marketing, among others). Despite these precedents, in practice there is still much uncertainty regarding the configuration of associative agreements.

Under the terms of the resolution, agreements with a duration of two years or more that establish a joint enterprise to conduct an economic activity shall be considered associative agreements, provided that the agreement establishes sharing of risks and results of the economic activity that makes up its subject matter and, cumulatively, the parties are competitors in the relevant market subject to the agreement. These agreements must be reported to and approved in advance by CADE when at least one of the parties’ economic group involved had gross revenues or volume of business in Brazil equal to or greater than R$ 750 million in the year prior to the transaction, and another economic group involved had revenues or volume of business in Brazil of at least R$ 75 million.

Cade has addressed the requirements of joint enterprise and sharing of risks and results, which involve a high degree of subjectivity, in a number of merger reviews thus far.

Regarding the first requirement, the agency found the existence of a joint enterprise depends on the degree and manner in which the cooperation is exercised between companies. In this regard, Cade considered that there was a joint enterprise, for example, in agreements that established coordination of the parties to market and sell a specific product; influence of one party on the business decisions of another; coordination of relevant issues related to the offering of products/services, such as quality, prices, and other commercial conditions involved in the deal; interdependence in the provision of services; and some types of governance structures to discuss relevant issues and regulate joint decision-making. In addition, Cade noted in some precedents that the concept of a joint enterprise is directly linked to the idea of conducting an economic activity, since the associative agreement must specifically address the acquisition or supply of goods or services in the market.

With regard to the sharing of risks and results, the case law indicates this requirement goes beyond profit or cost sharing. Cade has already understood that mere cost sharing is not enough to meet this requirement Sharing of risks and results is not to be confused with the mere existence of income, revenues, and losses from an accounting point of view. This requirement will be met when it is possible to identify participation by one party in the results obtained by the other, such as payment for performance or based on sales revenue of the party receiving the supplied products . Sharing may be implicit in the purpose of the agreement, for example, when two companies coordinate to expand their services, share capacity, or minimize costs, and ultimately dilute the risks associated with the business.

Cade further analyzed in other cases, a more objective requirement provided in the Resolution – which is the competitive relationship between the parties in the relevant market subject to the agreement, that would be satisfied even in the event of potential competition between the parties. This position was adopted in at least two precedents involving the pharmaceutical industry where the products subject to the agreements were not yet marketed in Brazil or were still under development (pipeline) but were conservatively considered potential competitors of the products already marketed by the other party in Brazil.

Cade's position in this set of cases establishes some guidelines that help, to some extent, to assess the need to report associative agreements in specific situations. However, this task is far from trivial, as the agency's understanding is closely linked to the content of certain contractual provisions, which are generally kept confidential. This makes it hard to fully understand the reasoning supporting the agency’s decisions. In addition, contractual relations between economic agents have increasingly diversified and innovative content, which makes the assessment of mandatory submission to Cade's scrutiny even more complex.

- Category: Infrastructure and energy

After more than six years under discussion, Bill No. 6,407/13 (the Gas Bill) was approved by the Chamber of Deputies' Mines and Energy Committee on October 23rd. The text amends provisions of Law No. 11,909/09, which establishes the legal framework for the natural gas sector in Brazil.

With this approval, the Gas Bill will now pass on for review by three other committees of the Chamber of Deputies: that of Economic Development, Industry, Trade, and Services; Finance and Taxation; and Constitution and Justice (unless the case is placed under a regime of urgency, and the Bill goes directly for a floor vote). After final approval by the committees, the bill will be submitted to the Senate for review.

The text approved by the Mines and Energy Committee preserved most of the latest amendments to the bill, presented on the same day as the approval. Among the modifications, the exclusion of article 45 from the amended version stands out. The provision provided that the share of natural gas thermoelectric power in Aneel auctions should take into account the cost and availability of fuel traded by natural gas distributors. In the final text, definition of the ceiling prices for thermoelectric energy would be assigned to the Energy Research Company (EPE). According to the deputies, the prior wording of the article was contrary to the main motivation of the Gas Bill, which is the opening of the market.

Among the main modifications brought in by the Gas Bill, the following stand out:

- The implementation of an entry and exitmodel for contracting transportation capacity . Within the current legal framework, natural gas transportation has transportation models known as the postal or point-to-point model, where the molecule's path from the point of entry into the system to the point of exit is relevant for the gas transportation agreement. In the new model proposed by the Gas Bill (entry and exit model), the physical flow of the gas molecule is delinked from its contractual flow. With this new model, common in the European market, the ease of trading at distant points in the network should generate greater liquidity in the natural gas market.

- The application of the regime of authorization for the transport and storage of natural gas. Currently, the activity of transportation of natural gas may be carried out pursuant to a concession (for new pipelines) or pursuant to permit (for existing pipelines or those being deployed at the time of enactment of the law). However, due to the bureaucratic difficulties of the concession model, no pipeline has been built or operated pursuant to a concession since the enactment of the current law. Under the new framework intended, the activity of transportation of gas will no longer be carried out pursuant to a concession, only permits. Similarly, underground storage of natural gas will now be performed under the permit regime with a future promulgation of the Gas Bill.

- The unbundling of the activities of transportation of natural gas from other activities in the industry. In order to curb self dealing and preserve competition in the industry, the Gas Bill contains a provision that prohibits natural gas carriers from directly engaging in competitive activities in the industry (trading, production, liquefying, and importing) or from having direct or indirect ownership interest in companies that perform these activities. The unbundling of market players is already a reality in Brazil in the regulation of the electricity sector.

- The creation of market areas and reinforcement of the issue of organization of gas transport in a network. Although it no longer provides for the creation of a specific agency to coordinate gas transportation throughout the Brazilian territory (similar to the ONS in the electric energy industry), as had been discussed in the Gás para Crescer [“Gas to Grow”] initiative, the Gas Bill has provisions for market areas, coordinated by a market area manager. The Gas Bill also has self-regulatory mechanisms in order to put into operation the interaction between industry players and transport network control (such as common network codes created by market area managers).

- Expansion of the list of infrastructure considered essential. In the current legal framework, only transport pipelines are treated as essential facilities. This means that their operators/owners must grant access to these facilities to interested third parties through regulated access. Although it has not proposed regulated access to other infrastructure, the Gas Bill, based on the doctrine of essential facilities (already present in Brazil in industries such as electricity, railways, and telecommunications), provides for negotiated and non-discriminatory access to other structures in the industry (i.e., outflow pipelines, processing units, LNG terminals, and their respective gas pipelines). This change also seeks to increase the competitiveness of the industry to prevent the reserve of the market by the owners of these infrastructure items.

Despite the changes brought in by the Gas Bill for implementing the new model for purchasing transport capacity for entries and exits, article 44 of the Bill itself ensures preservation of the economic balance of the contracts in force at the time of the promulgation of the new law.

- Category: Litigation

With the extinction of so many airlines in Brazil over the last 20 years, it is essential to conduct an analysis of the factors that led these companies to fail, one after the other, unable to reorganize financially in order to continue operating in the market.

TransBrasil, in 2002, Viação Aérea de São Paulo (Vasp), in 2008, and Viação Aérea Rio Grandense (Varig), in 2010, are examples of large airlines that were declared bankrupt. They all filed for judicial reorganization, which ended up being converted into bankruptcy. In 2007, BRA Transportes Aéreos also requested the processing of its judicial reorganization and then permanently suspended all its flights and sold its aircraft.

The most current case of this kind is that of Oceanair Linhas Aéreas, known as Avianca Brasil, which filed for judicial reorganization in December of 2018 and has since faced serious financial difficulties that cast doubt on its effective ability to continue operating in the market. Of concern are the significant number of laid-off employees, high indebtedness, the repossession by lessors of most of the company's aircraft, and the uncertain existence of assets, even more so after the redistribution of their slots (flight schedule for take-offs and landings at airports) by the National Civil Aviation Agency (Anac).

It is undeniable that high operating costs are a relevant factor for the difficulties that airlines face. To make up their fleet, for example, they need to purchase or lease aircraft that are expensive and subject to exchange rate variation and have high maintenance costs. As an aggravating factor, they still suffer from the high competitiveness in the civil aviation market, translated into ticket price wars.

These factors, however, are not the only ones behind the financial difficulties faced by airlines. To understand the problem further, one needs to look closely at the legal issues surrounding the subject.

When the processing of judicial reorganization is granted to a company, all existing actions and executions against the debtor are suspended for a period of 180 days (article 6, paragraph 4, of the Judicial Reorganization and Bankruptcy Law - LRF). During this period, it is prohibited to remove from the debtor’s place of business “capital assets essential to its business activity” (article 49, paragraph 3, of the LRF).

In the judicial reorganization of airlines, however, the LRF establishes a relevant exception: leased aircraft may be retaken at any time by the lessors, who are their actual owners, in the event of default on the consideration due for the use of the aircraft. That is, the lessors do not have their rights suspended (article 199, paragraph 1, of the LRF), even though the aircraft are well known to be the most essential assets for the airlines’ activities.

Although it seems contradictory, there is no antinomy or conflict between the rules. In fact, the LRF has established a specific and peculiar scenario in which the legislator's intent was to remove absolutely unviable airlines from the judicial reorganization system - those which, in addition to not being in minimum conditions to acquire their own aircraft to make up their fleet, they do not even have the financial capacity to keep up with the payments for the lease of aircraft.

This debate arose this year in the context of the judicial reorganization of Avianca Brasil. The trial judge chose to mitigate the exception expressly provided for in article 199 of the LRF, which gives the lessor the right to immediately retake the aircraft in the event of default on the lease, by virtue of the principle of preservation of the company and the social function of contracts. After several months of suspension of the lessors' rights, however, the São Paulo Court of Appeals (TJ-SP) reinstated the application for the exception provided for in the LRF, thus allowing for the immediate reinstatement of possession of the aircraft, regardless of the impact this measure would have on Avianca Brasil. The decision was based on the assumption that if the company does not have the resources to continue to regularly perform under lease agreements, maintaining its business activities would no longer be viable.

In this case, in addition to not being able to repossess their aircraft for several months, the lessors had to allow Avianca Brasil to use their assets without any consideration.

The situation worried the lessors and the international aviation market, as it spread fears that, in Brazil, airlines could use the judicial reorganization system as a means of transferring the risks of their commercial activities to aircraft lessors. This would make the costs and charges resulting from lease agreements in Brazil more costly and would have negative consequences for other Brazilian airlines and consumers, to whom part of these costs is passed on.

Avianca Brasil's case also had repercussions in the international legal community, as it also represented violation by Brazil of the Cape Town Convention. Upon formalizing its adherence to this treaty, Brazil promulgated Decree No. 8,008/13, pursuant to which it opted for “Alternative A” provided for in the convention. Under this alternative (article XI(2) of the treaty), in a scenario of insolvency, the airline is required to return aircraft subject to a non-performing lease within 30 days. As the case of Avianca Brasil represented the first airline reorganization after Brazil's accession to the Cape Town Convention, the repercussion was negative, and the Brazilian Judiciary was seen as being in breach of international treaties.

Following the return of the aircraft to the lessors and the redistribution by Anac of Avianca Brasil’s slots, the company's financial difficulties worsened. With the suspension of commercial activities and the absence of relevant assets that could ensure the continuity of operations, the TJ-SP then considered converting the judicial reorganization into bankruptcy, even though the judicial reorganization plan had been approved by the creditors. However, by a majority opinion, the TJ-SP found that the conversion, sua sponte, of the judicial reorganization into bankruptcy was impossible, given the absence of an express request by the lessors, who had only challenged the legality of the judicial reorganization plan submitted by Avianca Brasil (Interlocutory Appeal No. 2095938-27.2019.8.26.0000 filed by Swissport Brasil Ltda. and Interlocutory Appeal No. 2098259-35.2019.8.26.0000 filed by Petrobras Distribuidora S/A).

The case reinforces the idea that, once the return of the aircraft to the lessors is ordered, the airlines are unlikely to be able to lift themselves. The alternatives available are only the conversion of the judicial reorganization into bankruptcy or the termination of commercial activities. This is mainly due to the fact that the airlines were late in filing for judicial reorganization, only when they were already in a dramatic and unsustainable financial situation, where there was no possibility of resuming commercial activities and insolvency was irreversible due to the high degree of indebtedness.