- Category: Real estate

In Rio de Janeiro the deadline for payment of the balance of the Urban Property Tax (IPTU) and the Home Garbage Collection Tax (TCL) for the year 2020 ends on June 5, with no increase for arrears and with a 20% discount. The incentive was granted by Municipal Law No. 6,740/20, signed by the mayor on May 11 as part of the measures to alleviate the impact of the covid-19 pandemic.

Bills due or open until the date of publication of the law may be paid in a single installment. For bills due or falling due up to the month of July of 2020, the payment may be made, without additions for arrears, within up to five monthly installments starting in August, provided that the amount of the installment is greater than R$ 50.00.

Law No. 6,740/20 provides that the benefits have no retroactive effect and that no amount relating to the IPTU or TCL for the fiscal year 2020 paid previously will be refunded, even for those who have already made full payment of the IPTU for the fiscal year 2020 with the discount of 7% at the beginning of the year.

To qualify for the benefit, interested parties should request the discount from the Municipal Treasury Department (SMF) using the application available at the Carioca Digital website (https://carioca.rio/) by June 4 (for full payment) and by August 30 (in the event of installment payment). Taxpayers who seek to make installment payments can also submit the request by e-mail to

Law 6,740/20 also brings about benefits for taxpayers in the hotel sector, including inns and hostels. In their case, IPTU tax debts may be discharged with a discount, whether or not they are registered as outstanding debt, when their triggering event is prior to 2020 and they do not meet the conditions for the 40% reduction set forth in article 3 of Municipal Law No. 3,895/05, which grants tax benefits to hotels. The discounts are up to 40% on the amount of the tax due and up to 80% on the default charges, by means of a single payment, in cash, by the last business day of August of 2020.

The forms for payment of debts not registered at outstanding debt will be available on the SMF website until August 21. To look up, pay in cash, or obtain an installment plan for debts registered as outstanding debt, hotel taxpayers must access Carioca Digital (https://carioca.rio/).

In addition to benefiting taxpayers with a significant discount to settle their tax debts, the measure is also an attempt by the city government to minimize the effects of the significant drop in tax collection observed during the pandemic.

- Category: Labor and employment

This guide summarizes procedures that your company should follow to resume activities safely.

In it, you will find information about:

- How to identify activities that can be resumed

- Prior preparation of the working environment

- Measures to be maintained during the pandemic

Click here to see complete guide.

- Category: Tax

Virginia Pillekamp, Fernanda Sá Freire Figlioulo e Ana Yoshie Yassuda

A recent position of the Federal Supreme Court (STF) established a new chapter in the dispute among the states of the federation over the competence to charge ICMS tax on imports, the so-called "war of the ports.” When ruling on Extraordinary Appeal with Interlocutory Appeal No. 665134 (ARE 665134), on April 27, the STF unanimously established the following theory of General Repercussion (topic 520):

"The taxing authority for the ICMS tax obligation levied on imported goods is the member state in which the legal recipient of the transaction that gave rise to the circulation of the goods is domiciled or established, with the transfer of domain."

The theory justifies the declaration of partial unconstitutionality, without a reduction in the text, of article 11, I, "d" of Federal Supplementary Law No. 87/96 (Kandir Law), which defined the establishment of the "physical entry" of imported goods or merchandise as the place of the operation or delivery, for the purposes of ICMS taxation due on importation (ICMS-Import).

The theory is important in determining the taxing authority of the ICMS, especially in the context of the “war of the ports." To optimize the tax and financial aspects of import operations, Brazilian companies sought to perform the customs clearance of goods and merchandise through trading companies located in states of the federation with more favored taxation, which would then be the taxing authorities of the ICMS-Import tax.

The war of the ports affected the sector when the tax authorities of other states of the federation, such as São Paulo and Minas Gerais, issued thousands of fines against these companies, based on the aforementioned provision of the Kandir Law. With the STF's position on this topic, the location of the "physical entry" of goods becomes irrelevant in determining the taxing authority for the ICMS-Import tax.

In the vote of the reporting judge, Edson Facchin, it is possible to perceive three topics of majority reasoning in the composition of Topic 520.

First, the STF held that the definition of the taxing authority of the ICMS-Import tax obligation is based on the final recipient of the goods, which is not interdependent on the place of customs clearance:

"Therefore, customs clearance is the temporal aspect of the event of levy, being, it bears repeating, a criterion unrelated to the definition of the personal aspect of the tax obligation."

In agreement with this observation, the Justice highlighted the concept of a "final recipient" for that context "(...) that gives cause for the occurrence of the circulation of goods, characterized by transfer of domain." And, thus, as for "circulation of goods", Edson Facchin emphasizes that, provided that there is actually an international legal business, for the purposes of defining the establishment responsible for the tax, this expression includes the physical entry and symbolic entry of imported goods. In symbolic entries, this determination is based on the understanding that there is legality emanating from a documental or symbolic operation in feigned circulation of goods, provided that there is an actual legal business.

To demonstrate the proposed understanding applied to the three most common scenarios of importation of goods in the Brazilian legal system, the Justice explicitly outlines three interpretative guidelines, according to his own words, expounding them in topics:

- a) In importation on its own account, the economic recipient coincides is the same as the legal recipient, since the importer uses the goods in its production chain;

- (b) In importation to the account and at the order of a third party, the legal recipient is the one who gives actual cause for the import operation, that is, the party contracting for the rendering of services consisting of the performance of the customs clearance of goods, in its own name, by the importer contracted; and

- c) In importation to its own account, to order, the legal recipient is the importing company (trading company), because it is the one who engages in the ICMS triggering event with the intention of subsequent resale, even if per a prior agreement, after the process of internalization.

Establishment of the theory, according to Justice Edson Fachin, provided legal security to import operations, supporting and clarifying the STF's understanding, as well as stabilizing social expectations on legal relationships of a tax nature.

Assessing the specific case, we believe social expectations remain unstable. To explain better, in the case put under analysis in ARE 665134, clearance of the goods occurred in the state of São Paulo, followed by the sending of the materials in transfer to the state of Minas Gerais for the industrialization process. Later, the goods returned to São Paulo for marketing and sale.

In promoting the debate, the taxpayer argued for the levy of the tax in São Paulo, alleging, among other issues, that the establishment located in Minas Gerais had the objective of enabling the industrialization of raw materials to order in a brokerage stage only. Thus, since the final recipient of the imported goods is located in São Paulo, the ICMS tax should be pay to the São Paulo tax authorities.

The STF held that the taxing authority of the ICMS-Import tax was the state of Minas Gerais, despite the fact that, in the headnotes and in so many other passages of the opinion, it argued that "the economic recipient should not be confused with the legal recipient. Due to this contradiction, among other aspects of the decision, the taxpayer, on May 25, 2020, filed a motion for clarification, which is pending review.

- Category: Litigation

On May 21, the House of Representatives approved Bill 1,397/20, which contemplates emergency measures to deal with the effects of the covid-19 pandemic, including amendments to the Bankruptcy and Corporate Reorganization Law (LRF). The approved version has some changes in relation to the original proposed by Representative Hugo Leal.

The text under consideration in the Senate makes it clear that all the provisions it contains apply to legal entities under private law and to individual businessmen, and the mechanisms of legal suspension and preventive negotiation can also be used by rural producers and self-employed professionals who regularly carry out their activities. Bill 1,397/20 states, however, that its measures do not apply to consumers and to cooperative acts performed by cooperatives with their members.

Unlike the original version, which extended the duration of the transitional measures until the end of the pandemic, the version of the Bill approved provides that they will be in force from the publication of the law until December 31, 2020. The transitional measures created by Bill 1,397/20 are:

- Legal suspension: period of 30 days from the effective date of the law (in the original version is was 60 days) during which legal actions of an execution nature involving discussion or performance of obligations due after March 20, 2020, as well as contract revision actions, are suspended automatically.

The following acts relating to contracts signed or renegotiated before March 20, 2020, are also prohibited in such period:

- judicial or extrajudicial executions of real, fiduciary, secured, and co-obligation guarantees;

- decrees of bankruptcy;

- unilateral termination of bilateral contracts, thus considering null and void any contractual provision to that effect, including early maturity.

However, this prohibition does not apply to obligations arising from claims of a strictly salary nature, to contracts entered into after March 20, 2020, or to the exercise of rights of early maturity and offsets in the scope of repo and derivative transactions.

The approved version of the bill provides, unlike the original, that no late fee (contractual or tax) will be imposed. As nothing is said about default interest and adjustment for inflation, it is possible to argue that such charges will apply.

- Preventive negotiation: a procedure of voluntary jurisdiction, which may be filed, within 60 days of the end of the period of legal suspension, by economic players who have a reduction of 30% or more of their turnover compared to the average of the last quarter, as attested by an accounting professional.

The assignment of the claim to a court, which must be submitted to the court of the place of the debtor's principal place of business, will entail suspension of executions against the debtor for a maximum and non-extendable period of an additional 90 days. The debtor maintains the protections applicable to the legal suspension period discussed above. Once the claim has been assigned to a court, the competent judge will examine whether the formal requirements for the benefit have been met, thereby ceasing the suspension and terminating the proceedings if they have not been met.

No response, brief, or any kind of inquiry or expert investigation regarding the claim for preventive negotiation shall be entertained.

During these 90 days, the debtor must seek to renegotiate out of court the terms and conditions of its debts. The position of a negotiator previously provided for was excluded from the approved version of the bill. At the end of this period, the debtor must notify the judge of the result of the negotiations within 60 days. The case will be shelved after the submission of this report.

The bill establishes that, in the event that a petition for judicial reorganization is filed thereafter, the legal suspension period shall be deducted from the 180-day stay period already provided for in the LFR.

A novelty of the approved version of the Bill is that creditors who have entered into an settlement with the debtor during the legal suspension or preventive negotiation period will have their rights and guarantees originally contracted restored if the debtor applies for judicial or extrajudicial reorganization within 360 days of the execution of such settlement.

The bill makes it clear that the debtor may enter into, regardless of judicial authorization, financing agreements and receivables discounting operations with any financing agent, investment fund, including its creditors, partners, or companies in the same economic group, to fund its restructuring and preserve the value of its assets.

The novelty of the bill approved by the House of Representatives is treating as not subject to judicial and/or extrajudicial reorganization the debt claims arising from financing and discount agreements provided between March 20, 2020, and the end of the validity of the law. In the event of bankruptcy, such a debt claim will have the priority provided for in subsection V of article 84 of the LRF.

- Provisional amendments to the LFR (applicable only to proceedings initiated or amended during the term of the law proposed by Bill 1,397/20): for requests for judicial reorganization and approval of out-of-court reorganization plans initiated during the term of the law, the bill proposes relaxation of certain requirements, such as allowing new requests by companies that have already benefited from these institutes without time restriction and reducing the quorum for approval of out-of-court reorganization to a simple majority of the creditors involved (currently three-fifths).

During the transitional arrangement, an application for approval of an out-of-court reorganization plan may be submitted with proof that creditors representing at least one third of all the claims of each type covered by the plan have agreed to it, with a commitment to reach the quorum referred to above within a non-extendable period of 90 days from the date of the application. The creditor may also convert the application into judicial reorganization.

The bill also provides for the granting of a stay period to the debtor applying for extrajudicial reorganization in view of the type(s) of creditor(s) covered. As we indicated in our prior article, the LRF does not provide for a suspension period for this type of proceeding, but case law already allowed for it.

In the case of bankruptcies, the minimum default limit for bankruptcy to be decreed was raised from 40 minimum wages (i.e. R$ 41.8 thousand)1 to R$ 100 thousand.

The transitional rules proposed in the bill also affect ongoing out-of-court reorganization, judicial reorganization, and bankruptcy proceedings: obligations assumed in ratified reorganization plans will not be payable for 120 days, and during this period the possibility of conversion of reorganizations into bankruptcy due to noncompliance with the obligations established in approved plans is suspended.

In addition, debtors may submit a proposal for a new reorganization plan including debts that were taken on after the assignment to a court of the application for reorganization, which is currently prohibited. The approved version of the bill excepted debt claims related to financing granted during judicial reorganization, known as DIP financing, but limited them to those that had been preceded by the express consent of the Judiciary. The legislature's choice in this regard is controversial, since the granting of this type of financing today does not require judicial consent under the current system.

The bill also stipulates that debtors will be entitled to a new stay period under the LFR.

With regard to the addition to the plan, the amount of the claims originally held by the creditors, less any amounts paid, shall be taken into account both for the calculation of the amount to be paid and for the counting of votes for approval of the amended plan.

For micro and small businesses, the bill establishes more beneficial rules for the debtor in the event of judicial reorganization, with a special plan providing for payment of the first installment within one year.

As the text was approved by the House of Representatives, the administrative acts of nullification, revocation, blocking of registration, or registration of taxpayer numbers that are subject to judicial discussion in the scope of judicial reorganizations are suspended during the term of the law.

In our next article, we will examine the possible changes proposed for the text of the Bill by the senators.

1 Based on the national minimum wage in force on the date of publication of this article (R$ 1,045.00), as provided for in Executive Order No. 919, of January 30, 2020.

- Category: Labor and employment

The Federal Supreme Court (STF) en banc has partially approved an in limine decision issued by Justice Marco Aurélio de Mello as reporting judge for seven Direct Unconstitutionality Suits (ADIs) filed against Executive Order No. 927/20 and suspended the understanding that covid-19 is not an occupational disease. The decision was reached by a majority vote in a session held on April 29.

The Justice writing for the court, who had rejected the preliminary injunction requested by the parties and the workers' representative entities, voted to maintain his decision. However, the dissenting opinion opened by Justice Alexandre de Moraes prevailed, to the effect of suspending article 29, which does not consider contamination of workers with the coronavirus to be an occupational illness, except when the existence of a causal link between the illness and work has been proven. Article 31 was also suspended, according to which labor inspectors must act in a guiding manner with respect to irregularities found during the 180-day period when the Executive Order came into force.

For most of the Justices on the STF, the requirement that the employee prove a relationship between coronavirus contamination and work imposes "diabolical proof," given the impossibility of precisely defining in which circumstance the disease was contracted. The decision, therefore, signals that it would be the employer's burden to prove that the disease was not acquired in the work environment or because of it, thus reversing the burden of proof in the specific case of infection with the coronavirus.

The main implications of recognition of an occupational illness are suspension of the employment contract and the right to provisional job security for a minimum period of 12 months.

Considering the dizzying increase in the number of people infected with the coronavirus in Brazil and the economic impacts of the pandemic, a temporary guarantee of employment for workers who contract the disease places an even greater burden on companies, which are already being forced to lay off employees or even close down their activities.

In addition, if the STF's understanding is maintained and employers are unable to prove the absence of a causal link between contamination with the coronavirus and work, there will be an increase in taxation on companies due to the impact on the calculation of the Accident Prevention Factor (FAP).

For that reason, it is recommended that companies submit an appeal in the administrative sphere, in the event that accident illness aid (type B-91) is granted to workers placed on leave due to covid-19 in order to convert the social security benefit into common illness aid (type B-31). The absence of a causal link between contamination and work must be demonstrated through evidence of the adoption of mandatory measures, in addition to the guidelines and recommendations of the Brazilian authorities to confront the pandemic.

Similarly, in labor claims, if there is a request for recognition of an occupational illness by a worker contaminated with the coronavirus, companies must handle the case like any other request for recognition of an occupational illness. To this end, they must submit documents proving the adoption of individual and collective protection measures to preserve the health of their employees and request medical expert evidence, including at the workplace.

It is important to remember that the Social Security Benefits Law (Law No. 8,213/91) provides in its article 20, paragraph 1, "d", that endemic disease is excluded, as a rule, from the concept of an occupational disease. The law considers a disease to be occupational only when it is proven that the contamination resulted from direct exposure or contact determined by the nature of the work.

Based on this provision, the precedents of the Labor Courts do not consider cases of contamination of employees by endemic diseases, such as malaria or leishmaniasis, to be occupational, precisely because of the impossibility of determining the time and place of infection. Labor case law finds an occupational nature only in cases where the workplace puts the employee at permanent risk to the vector of the disease or where there is displacement from a place where there was no risk of contracting it in order to fulfill the contract in a region prone to its development.

Although article 20, paragraph 1, "d" of Law No. 8,213/91 specifically governs endemic diseases, it is reasonable to apply the same understanding, by analogy, to covid-19, since the motivation for the rule is even more fitting in a pandemic scenario: difficulty in establishing when and where contamination occurred.

Therefore, based on the interpretation of this passage of the law and the principles of protection of the work environment, although the STF may declare in a final judgment the unconstitutionality of article 29 of MP 927/20, we believe that the cases of workers contaminated by the coronavirus whose employers have adopted preventive measures to contain the disease and complied with the workplace health and safety rules, in addition to the guidelines of the health authorities, cannot be classified as occupational.

- Category: Tax

The covid-19 pandemic led various commercial, industrial, and service providers in Brazil to suspend their activities indefinitely. Thus far, there is no prospect of normalization of economic activity.

Although some activities can be carried out remotely, in other sectors it is common for employees to be dismissed from work while social distancing measures last. In such cases, employees do not work, but maintain their employment relationship and continue to receive the amounts usually paid by the employer. This may be the case, for example, with shop assistants or with workers of large industrial plants, activities that cannot be performed remotely.

Situations in which employers continue to make payments to employees, even when they are dismissed from work, may give rise to the non-imposition of the social security contributions due by the employer on these amounts. This is because section 22, subsection I, of Law No. 8,212/91 provides that the employer's social security contributions shall be levied on compensation paid, due, or credited to the workers and intended to compensate work.

The compensatory element thus assumes a central role in defining the scenarios for the imposition of social security contributions. These social contributions become due only if the payments serve as compensation for the service provided or for the availability of the service provider. In other words, if the employee is not being compensated for providing services or for being at the employer's disposal, then such payments should not be subject to the social security contributions due by the employer.

Accordingly, the Superior Court of Justice (STJ) ruled, under the repetitive appeals procedure (REsp 1.230.957/RS), that no social security contributions are levied on amounts related to indemnification for the lack of dismissal notice paid to employees, since there is no retributive element in the payment. We believe that this STJ decision reinforces the importance that there must in fact be compensation for these social security contributions to be levied.

More recently, the Federal Prosecutor's Office has expressed a similar view in Extraordinary Appeal 1.072.485/PR, defending the non-imposition of the social security contributions due by the employer on the additional vacation pay, precisely because such cases also do not involve compensation for the provision of services, among other reasons.

Although tax authorities may adopt a different position from that set forth above, in our opinion, it is possible to argue that employees in this situation are not at the employer's disposal if the employer is prevented from operating in a normal manner, whether due to health measures to preserve the health of employees or due to municipal and state regulations. Thus, when it is impossible for employees to perform the activity for which they were hired, we believe that it cannot be said that they are at the disposal of their employer.

In the case of employees who have been dismissed as a result of the pandemic, but maintaining the employment contract, there does not seem to be any payment for the time that the employee remains at the employer's disposal, since there is no prospect of a return to normality and regularization of the activities of these employees. In fact, employers do not seem to take advantage of this potential availability of employees, since economic activity cannot be resumed while the restrictions continue. That is why it is unlikely that this is the reason for maintaining jobs and making the payments discussed here.

The preservation of jobs at this time seems to be more related to the high costs for the formal dismissal and subsequent hiring of employees, or even the laudable feeling of social solidarity, than to the expectation that the provision of services by employees will be necessary again in the short term. In this context, amounts paid by employers to employees who are dismissed from work are similar to the arrangement for cost allowances, expressly dissociated from compensation by section 457, paragraph 2, of the Consolidated Labor Laws, and on which no social security contributions due by the employer are imposed.

In view of the above, we believe it is possible to question the imposition of the social security contributions due by the employer on the amounts paid to employees dismissed from work due to the covid-19 pandemic.

- Category: Infrastructure and energy

The serious economic consequences of the covid-19 pandemic put the organization and management capacity of Brazilian regulatory agencies to the test, in addition to requiring adjustment of standards to mitigate the impacts in some extremely relevant sectors. This is the case of the air sector, one of the most affected by recent economic, social, and health changes.

With most aircraft out of service and a drastic reduction in passenger demand, airlines are experiencing an unprecedented crisis around the world. In Brazil, the National Civil Aviation Agency (Anac) has been proactive and sensitive to this delicate moment, taking a series of measures to mitigate the negative economic consequences of the sector's almost complete shutdown.

Besides authorizing the transportation of cargo in the passenger cabin, Anac’s board of directors recently approved two new resolutions that have as their main objective facilitation of the operation of the companies and to grant a brief financial respite that may be decisive for the future of some companies in the sector.

Resolutions No. 556 and 557 temporarily amend some provisions of Anac Resolution No. 400, which establishes the general conditions for air transport in Brazil. According to the new standards, the following rules shall apply:

- If the carrier changes the flight schedule and itinerary in a scheduled manner, passengers must be informed at least 24 hours in advance of the originally contracted time. Before the modification approved by Anac's board of directors, the minimum deadline was 72 hours.

In cases of change, flight delay, cancellation of flight, or interruption of service, the carrier shall be exempt from the following obligations:

- Offering material assistance, provided that the change, delay, cancellation, or interruption has been caused by the closure of borders or airports as mandated by the authorities;

- Offer re-accommodation on another company's flight to the same destination at the earliest opportunity if there is availability on another carrier's own flight; and

- Offer provision of the service by another mode of transportation.

- In cases of delay of more than two hours, the transporter will not be obliged to provide meal vouchers or to observe the meal characteristics to be provided according to the schedule.

- Information requested by users must be provided and complaints resolved within 15 days, suspending the period of ten days originally stipulated by Anac Resolution No. 400.

The new rules apply to all flights originally scheduled or events registered by December 31, 2020.

Anac took the opportunity to draft the new resolutions to clarify the reimbursement rule in Executive Order No. 925. According to the text promulgated by the Brazilian President’s Office, the period for reimbursement of the purchase price of tickets is 12 months. However, Anac Resolution No. 557 clarifies that this deadline does not apply to cases in which the passenger withdraws and the request was made within 24 hours of receipt of the voucher, when the ticket was purchased seven days or more before the boarding date. In this case, the seven-day period for reimbursement provided for in Anac Resolution No. 400 remains in force.

Aviation is going through a delicate time and its survival will require the joint and coordinated action of the government, private initiative, and the regulator. The economic effects of the pandemic are still unpredictable, however, to reduce its reach, mitigation measures must be precise and timely.

- Category: Infrastructure and energy

The crisis caused by the covid-19 pandemic continues to hit various sectors of the economy relentlessly. In Brazil, the domestic air market has been reduced by 90%, while the international market remains practically shut down, according to data released by the National Civil Aviation Agency (Anac).[1]

A series of regulatory measures have already been implemented by Anac with the aim of providing financial breathing space for airlines and making some operational rules more flexible, in an attempt to guarantee minimum survival conditions for the sector during this period of extreme reduction in demand. Rules on reimbursement of tickets, transport of cargo in the passenger cabin, deadline for meeting consumer demands, and notice period for cancellations and rebookings were promulgated. However, thus far there has been no concrete position on issues of a health nature.

The gap in the guidelines involving official prevention measures was filled on May 19, with the publication of health measures for aviation. They are based on a technical note prepared by the National Health Surveillance Agency (Anvisa), which brings in a series of recommendations for airport operators, workers, civil servants, airlines, and service providers.

In addition to the already known recommendation for the use of face masks, Anvisa suggests the adoption of the following measures:[2]

Airport operators:

- Observe the guidelines of the World Health Organization (WHO);

- Intensify surveillance of suspected cases at airports so that the isolation measures necessary are taken and reporting to the relevant bodies is carried out;

- Disseminate audible warnings in all departure and arrival areas with the texts indicated by the health authorities;

- Notify the health authority of suspected cases identified in the airport area;

- Disseminate guidance on websites so that only passengers transit through terminals;

- Supervise cleaning teams to ensure the frequency of cleaning and disinfection of workers' personal protective equipment;

- Organize the movement of people in terminals in such a way as to allow a minimum distance of two meters;

- Increase the availability of hand sanitizer and liquid soap;

- Post informational materials with the prevention measures;

- Limit bus capacity to 50% of capacity in trips between terminals; and

- Keep the air conditioning systems with renewal of air at maximum capacity.

Airport civil servants and workers:

- Respect the minimum distance of two meters;

- Wash hands frequently with soap and water or, if not possible, use 70% alcohol sanitizer;

- Avoid touching the eyes, mouth, and nose;

- Clean hands after coughing or sneezing;

- If suspected cases are reported, wear an apron, goggles, and gloves in addition to a surgical mask; and

- Use personal protective equipment.

Airlines:

- Publicize audible warnings on all flights, as indicated by the health authorities;

- Supervise aircraft cleaning teams to ensure intensified cleaning procedures;

- Leave only security cards in the pockets of the seats and ensure the process of cleaning and disinfecting cards;

- Require crew and passengers to wear masks;

- Carry out the cleaning and disinfection procedures at each stopover before the new passengers board;

- Guide the disembarkation to ensure distance between passengers;

- Organize check-in and boarding procedures, respecting the minimum distance of 2 meters;

- Provide 70% alcohol sanitizer and liquid soap inside the aircraft;

- Take steps to ensure as much air renewal as possible inside the aircraft;

- Suspend in-flight services on domestic flights, or, if the company chooses to maintain services, prioritize food and beverages served in individual, sanitized packaging; and

- Respond to requests for lists of travelers and crew members to enable the authorities to investigate suspected cases.

The technical note also includes guidelines for air taxi companies, specialized aeromedical transport companies and health inspection teams. The implementation of the measures will be supervised by a special working group set up at the request of the Ministry of Infrastructure and coordinated by Anac.

Moments of extreme economic stress such as that caused by the pandemic bring about financial consequences that are still immeasurable in the short term. On the other hand, they end up creating a favorable scenario for revising economic, management, and operational models, in addition to significantly speeding up the normally lengthy and bureaucratic process of drafting new standards.

One lesson that the pandemic provided to regulated sectors was the possibility of quick regulatory readaptation, without prejudice to the quality of the work developed. The actions of Anac and Anvisa so far is proof that it is possible to work efficiently in the preparation and alteration of rules and that regulation does not need to be synonymous with bureaucracy and slowness. The circumstances, although unfortunate, made two regulatory agencies work together with the same objective: to reduce the rate of contagion and ensure the survival of an economic activity of significant relevance to the functioning of Brazil.

The only certainty amid the chaos caused by the pandemic is that aviation and all its procedures will be drastically altered in the near future until the transmission of the virus is controlled. Until then, the joint effort of the authorities, private sector, and population will be essential.

[1] https://www.anac.gov.br/noticias/2020/novas-medidas-sanitarias-em-aeroportos-e-aeronaves-reforcam-uso-de-mascaras-e-protecao-aos-passageiros-e-profissionais

[2] Technical Note No. 101/2020/SEI/GIMTV/GGPAF/DIRE5/ANVISA

- Category: Infrastructure and energy

Liliam F. Yoshikawa, Roberta Danelon Leonhardt, Carolina Castelo Branco, and Camila de Carli Rosellini

On May 18, the National Mining Agency (ANM) published Resolution No. 32, which changes the rules for inspection and safety of dams in Brazil, initially instituted by Ordinance No. 70,389/17 of the then National Department of Mineral Production (DNPM), which created the National Registry of Mining Dams and the Integrated System for Mining Dam Safety Management. In addition, on May 19, the House of Representatives unanimously approved Bill No. 550/19 of the Federal Senate, which amends the National Dam Safety Policy (PNSB), Federal Law No. 12,334/10, with the aim of increasing dam safety requirements.

The new resolution amends some provisions of the abovementioned DNPM ordinance and revokes article 15 of ANM Resolution 13/2019, which established regulatory measures for mining dams, notably those built or elevated using the so-called "upstream" method or by a method declared to be unknown.

Among the principal changes, the resolution provides that there will be an automatic change to “high” in the risk category of the dam in the following cases:

- detection of anomalies, such as those of a structural nature with reduced slope capacity and without corrective measures, rise in downstream areas with material loading, increasing flow or infiltration of contained material with the potential to compromise the safety of the structure, or the existence of cracks, rebounds, or slips with the potential to compromise the safety of the structure;

- failure to send the Stability Statement (DCE) within the six-month period between the 1st and 31st of March and the 1st and 30th of September, or a finding of non-stability of the dam;

- failure to achieve safety factors, including those determined by ABNT Technical Regulation No. 13,028; and

- structure classified as Emergency Level 1, 2, or 3.

Another change relating to preparation of the flood map. Previously, the developer had to prepare it to support the classification of the Associated Potential Damage (DPA) of all its mining dams, individually, within up to 12 months from the entrance into force of the DNPM Ordinance, with it being possible in some cases to even make use of a simplified study. With the new resolution, the flood map should be more detailed and will serve as an aid both in classifying the DPA and in supporting the other actions described in the Emergency Action Plan for Mining Dams (PAEBM). There has also been a change in the timeframe for preparing and sending the flood map according to the level of the DPA. The new deadlines are:

- High DPA: by December 31, 2020

- Medium DPA: by February 28, 2021

- Low DPA: by April 30, 2021

In addition, the ANM may, at its discretion, lay down separate deadlines and obligations provided for in the new resolution in exceptional and duly justified cases.

The rule also provides that the individual with the highest authority in the hierarchy of the company that signs the DCE together with the technical person responsible for its preparation must be a Brazilian or naturalized Brazilian citizen, a mandate not previously provided for by the DNPM Ordinance.

The following are highlighted as the main amendments to Bill No. 550/19, which amends the PNSB:

- prerogative assigned to the ANM to demand or not demand security, insurance, guarantees, or other financial or real guarantees from developers to repair damage to human life, the environment, and public property.

- requirement to immediately notify the oversight agency, the environmental agency, and the competent civil protection and defense agency of any change in the safety conditions of the dam that could result in an accident or disaster.

- mandatory Emergency Action Plan (EAP) for all mining tailings dams and dams with associated medium-level potential damage.

- revision of the amount of the fine (previously R$ 20 billion) to a minimum of R$ 2 thousand and a maximum of R$ 1 billion, plus compensation for the families affected.

- change in the provision for payment of royalties, i.e., the obligations to pay the Financial Compensation for Exploration of Mineral Resources (CFEM) to the municipalities affected were removed from the Federal Senate’s text, even if there is interruption in activities and cessation of production.

- exclusion of the provision for modification of Law No. 8,072/90 (Heinous Crimes Law) to classify as heinous the crime of environmental pollution resulting in death. In the text approved by the House of Representatives in the alternative, the chapter on administrative infractions was detailed, establishing deadlines for the handling of cases and types of penalties that can be applied to offenders.

The current context and legislative changes put pressure on mining companies to meet the new requirements and eliminate any dams built by the upstream method as soon as possible, giving greater effectiveness to the PNSB.

- Category: Banking, insurance and finance

The Central Bank of Brazil (BC) and the National Monetary Council (CMN) issued, in early May, rules governing the use of book-entry trade notes in order to provide more security for financial institutions to use bills to offer credit.

Following the trend of dematerialization of financial assets and securities[1] seen in the Brazilian market in recent decades, the new rules face the issue at two levels:

- CMN Resolution No. 4,815 deals with financing transactions based on book-entry trade notes; and

- BC Circular No. 4,016 regulates the bookkeeping activity of these securities, creating a series of rules aimed at providing greater security for their issuance, registration, settlement, and trading.

More specifically, CMN Resolution No. 4,815 regulates market receivables discounting operations carried out by financial institutions and loans guaranteed by those receivables.

The main change brought about by the rule for these transactions was the mandatory use of registered and book-entry trade notes under BC Circular No. 4016. According to article 4 of the resolution, financial institutions should require their counterparts, in particular forward sellers who wishes to accelerate their receivables, to issue book-entry trade notes in sales or services.

The trade notes issued or receivables to be created in the future (in the case of so-called "smoke credits”), the institutions to which payments will be made, and the conditions for release of funds paid by debtors of the trade notes, in the case of loans guaranteed by such securities should also be specified via contract (article 5).

Also according to the resolution, the commands in the registration systems or centralized deposit in which the trade notes will be registered must be made by the creditor financial institution (article 6), including exchange of ownership and creation and cancelation of liens and encumbrances.

BC Circular No. 4,016, in turn, provides the necessary support for trading with electronic trade notes to grow in scale, without prejudice to security for the parties and the financial system as a whole. For this purpose, the agents responsible for operating the electronic bookkeeping systems (bookkeepers) must obtain prior authorization from the BC (article 11) and ensure that, concerning trade notes, such systems allow (article 3):

- the performance of all appropriate acts of exchange;

- control of payments;

- trading and exchange of ownership, registration, and centralized deposit in systems authorized to operate by the BC;

- input of encumbrances and lines on trade notes in such systems;

- input of information regarding the transactions carried out, issuance of statements; and

- interoperability with other systems of the same nature.

In a complementary manner, such agents must also observe a series of minimum service and governance standards, including the creation of internal risk management policies, the performance of services with minimum operational reliability, and care for the quality of information recorded in conducting the activity, among other requirements provided for in article 7 of BC Circular No. 4,016.

Also, emphasis should be placed on[2] the provisions of BC Circular No. 4,016 which require association between the trade notes and the respective electronic invoice by the bookkeeper (article 3, sole paragraph) and registration of the trade note in a system for registration or centralized deposit authorized by the BC that interoperates with the others (articles 14 and 19). These requirements are seen as important tools to prevent fraud that was considered an obstacle to the development of this market, such as the issuance of "cold" or duplicate trade notes.

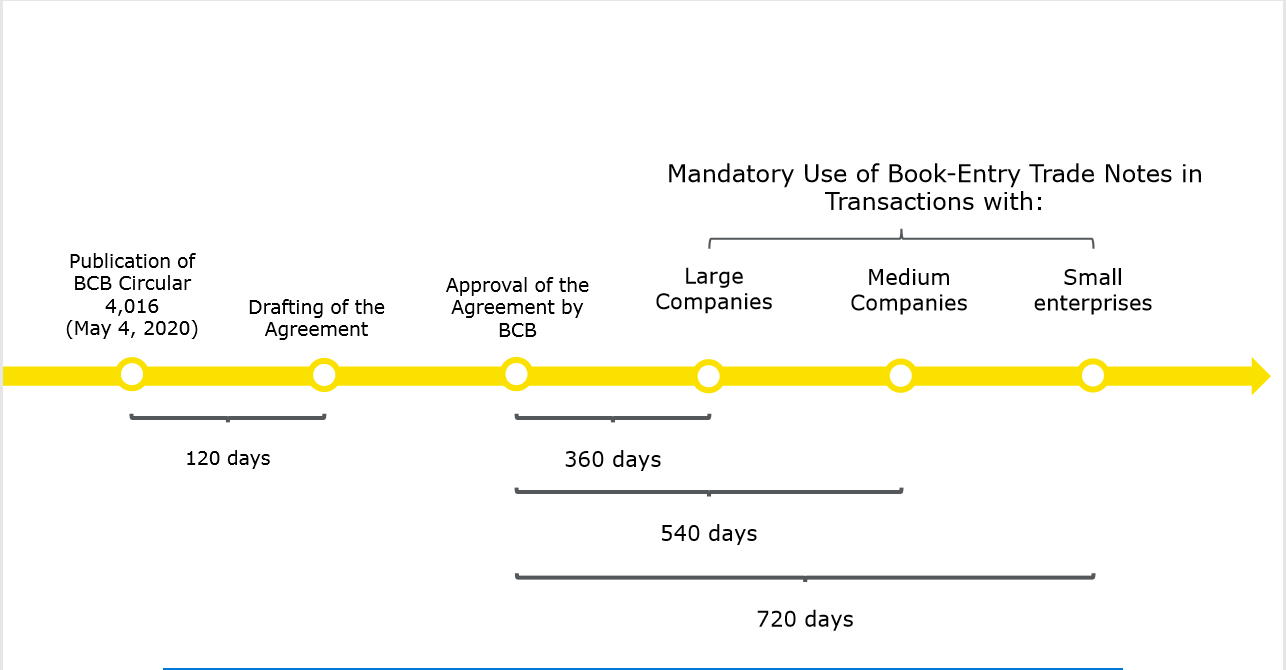

Considering the technical challenge represented by the implementation of these new systems, the mandatory issuance of book-entry trade notes for the negotiation of commercial receivables by financial institutions will only become effective after approval of the agreement between registrars and depositories provided for in BC Circular No. 4,016 and within deadlines that vary according to the size of the clients financed, as shown in the figure below (article 3 of CMN Resolution No. 4,815):

The system of book-entry trade notes established by BC Circular No. 4,016 and CMN Resolution No. 4,815 represents an effort to give this market security and robustness in the bookkeeping infrastructure already established by the national regulatory framework for other financial assets and securities. Figures such as bookkeeping agents, registration and centralized deposit systems, settling banks, and supervision closest to the BC itself may be new to the trade notes market in particular, but the fact is that this model and its effectiveness and solidity are already widely known by the financial market and its clients in general.

At the same time, applying these new rules to a segment as traditional as trade notes, with their own vices and virtues, may lead to the emergence of a set of new challenges, particularly cultural adaptation. Add to this the current unprecedented crisis resulting from the covid-19 pandemic, which makes it even more difficult to implement a technologically complex process.

In fact, security and predictability have their cost. But what is perhaps seen today as another concern by many can easily become a source of new opportunities. With significant adherence by financial institutions to loans and financing backed by book-entry trade notes, many companies will be able to access new, cheaper forms of credit. In addition, another opportunity is created for financial asset registrars. The financial market and its infrastructure providers therefore have the mission of adapting to this new regulatory reality and of seeking to achieve the objectives expected of them, which can certainly contribute to the resumption of economic development in Brazil.

[1] A more complete description of this process can be found in WELLISCH, Julya. “Títulos Nominativos: da Cártula ao Depósito Centralizado” [“Registered Securities: from Card System to Centralized Deposit”]. In: Revista de Direito Bancário e do Mercado de Capitais [“Review of Banking and Capital Markets Law”], vol. 66/2014, pp. 35-62.

[2] Other noteworthy provisions in the circular are the rules on the security of financial settlements relating to the payment of trade notes (Chapter III, Section II), minimum information to be made available to drawees (article 6), duties of the registration and centralized deposit systems (Chapter VI, Section I), and the execution of an agreement among the entities that manage them, which shall be prepared with the participation of the BC and deal with operational issues such as layouts and informational content of the files, procedures, times of exchange of information, fees, among others (article 20).

- Category: Infrastructure and energy

On May 18, the Federal government published Decree No. 10,350, which regulates Provisional Measure No. 950/20 and provides for the creation of an account for the energy sector to face the state of public calamity recognized by Legislative Decree No. 6/2020, called the Covid-Account.

The new decree seeks to mitigate the cash impacts suffered by distribution concessionaires as a result of the fall in energy consumption and increase in defaults caused by the covid-19 pandemic. According to article 1 of the decree, the Covid-Account will receive funds from the contracting of credit transactions with financial institutions. The objective is to cover deficits or accelerate revenues for energy distribution concessionaires.

The Covid-Account should alleviate the effects caused by the distributors’ over-contracting of energy and ensure neutrality of sectorial charges for distributors, among other repercussions. According to the first paragraph of article 1, the Electric Energy Trading Chamber (CCEE) is charged with contracting credit transactions intended to cover the Covid-Account, taking advantage of a lower cost of operation, since the Selic rate is now close to 3%, compared to 11% at the time of the creation of the ACR account, due to the crisis in the electric sector in 2014.

In order to receive the funds from the Covid-Account, distributors will have to expressly accept, on an irrevocable and irreversible basis, certain conditions, such as:

- prohibition until December of 2020 on requirements to suspend or reduce the volumes of energy acquired through power purchase agreements;

- limitation, in case of intra-sectorial default, on the distribution of dividends and interest on equity payments to the legal minimum percentage of 25% of net profit;

- the possibility of reimbursement by distributors of administrative and financial costs incurred in credit transactions and borne by consumers, subject to certain requirements; and

- waiver of the right to litigate, in a judicial or arbitral context, these conditions of acceptance.

It is not known whether all distributors will accept these conditions to receive the funds from the account, mainly because some of them generate discussions in the energy sector, such as limiting the distribution of dividends and interest on equity payments to the legal minimum percentage of 25% of net profit.

The costs of the financial transactions contracted will be passed on in full to the Energy Development Account (CDE, in Portuguese) and paid by consumers. Those who migrate to the free market during the financing period will not be exempt from paying the loan.

The decree also provides for the possibility of bilateral negotiation between distributors and Group A consumers, upon mentioning, in article 3, paragraph 3, subsection IV, that the amounts to be paid by the Covid-Account to the distributors will be approved by Aneel and will consider, among other factors, any deferred payment installments, by the distributors, of outstanding obligations related to the invoice of the demand contracted for Group A consumer units.

This possibility is in line with Order No. 1,406, of May 19, 2020, which, under Administrative Proceeding No. 48500.001841/2020-81, filed by Group A consumers, allows distributors to freely negotiate deferred payment installments of amounts related to invoices based on contracted demands instead of measured demands, under the terms of applicable regulations.

Although still subject to regulation by Aneel, the decree has been facing opposition, such as that of Legislative Decree Bill No. 231/20, filed by Federal Representative José Guimarães (PT-CE). The parliamentarian intends to halt the effects of the decree on the argument that there is no stipulation of a maximum amount for loans, which would mean a blank check to Aneel.

Although some of its points are controversial, Decree No. 10,350/20 constitutes an important emergency measure for the energy sector, since, as far as possible, it preserves the payment flow of the entire chain of the sector. It is not, therefore, a definitive solution to the problem, which is why it mentions that Aneel will be able to evaluate the need to restore the economic and financial balance of concession contracts, upon a justified request of the interested party.

- Category: Litigation

Bill No. 1,179/20, which adapts private law legal relationships (contractual, corporate, real estate, and agricultural, among others) during the covid-19 crisis, is proceeding for presidential signature. The matter was sent to the Office of the President for signature on May 21, and this is expected to occur by June 10 of this year.

The text approved follows the terms of the substitute presented by Senator Simone Tebet (MDB-MS) for the text initially prepared by the President of the Federal Supreme Court (STF), Justice Dias Toffoli, and presented by Senator Antonio Anastasia (PSD-MG).

The proposal approved is transitional and emergency in nature and considers the beginning of the pandemic to have occurred on March 20, 2020. In this spirit, the draft establishes a series of rules that modify Brazil's legislation on a transitional basis. Among other measures, the proposal:

- Suspends or prevents the running of the periods for peremption and the statute of limitations, from the entrance into force of the legislation until October 30, 2020.

- In the operation of legal entities, it establishes that, until October 30, 2020, face-to-face meetings and assemblies in the scope of associations, foundations, and companies must respect the health restrictions of the local authorities, expressly providing that general meetings may take place by electronic means, including for the purposes of statements and responses by participants, which must have the same effects as statements and responses with in-person signature, regardless of provision in the corporate documents of the legal entity.

- With regard to termination, rescission, and revision of contracts, it provides that the consequences arising from the pandemic will not have retroactive effects for purposes of default due to unforeseeable circumstances or force majeure, and that the impacts of inflation, foreign exchange rate variation, or devaluation and replacement of the exchange rate standard arising from this situation cannot be considered unforeseeable for the exclusive purposes of the Civil Code (force majeure, unforeseeable circumstances, or theory of unpredictability).

- In consumer relations, it establishes that the rules for arguing situations of force majeure, unforeseeable circumstances, acts of God, or theory of unpredictability cannot be applied in the context of consumer relations, in addition to suspending the right of buyer’s remorse and withdrawal periods for products and services delivered at home until October 30, 2020.

- In lease agreements, the granting of injunctions for eviction from urban real estate is suspended until December 31, 2020, within the scope of the eviction proceedings up to March 20, 2020.

- As for adverse position, accrual periods are suspended until October 30, 2020.

- In building condominiums, the owners association's powers are extended to restrict (a) the use of common areas to prevent covid-19; and (b) private areas for meetings, festivities, and the use of vehicle shelters by third parties. In no case may medical access and care be restricted. In addition, owners association meetings may take place on an emergency basis, in an electronic manner, whereby the statements and responses by the parties must also have the same validity as that done in person. All measures are also valid until October 30, 2020.

- In competition law, some practices prohibited by Law 12,529/11 are suspended (article 36, XV and XVII), among them (a) selling goods or rendering services unjustifiably below cost price; (b) partially or totally ceasing the company's activities, without just cause, while the other infractions of article 36 should be analyzed with a view to the pandemic situation, when performed during the period of applicability of the law. Finally, application of the provision that defines the execution of an association contract as an act of concentration (and article 90, IV, of Law No. 12,529/11 – article 21, of the Bill).

- In private paid transportation and delivery services by mobile phone application, there must be a reduction in the percentage of retention of the value of the trips by at least 15%, ensuring the transfer of this amount to the driver or deliverer.

- It establishes that the rules of the Brazilian Traffic Code may be relaxed by the National Transit Bureau (Conatran) to optimize efficiency in the logistics of transportation of goods and inputs and in the provision of services related to combating the effects of the pandemic.

- It provides that the effective date of the General Data Protection Law, for imposition of sanctions, will occur in August of 2021. Thus far, the effective date of the LGPD continues to be postponed to May 3, 2021, as per MP No. 959/2020, which is pending deliberation in the Brazilian Congress.

Senator Simone Tebet emphasized orally that the proposal does not deal with relations between consumers and public service providers, which depend on the actions of regulatory agencies, nor with bankruptcy and judicial reorganization issues, nor with labor or health legislation. These topics may be addressed in specific bills.

If the matter is vetoed, in whole or in part, by the Brazilian President, the bill will return to the Brazilian Congress for further deliberations.

Click here to see the infographic that summarizes the subject.

- Category: Environmental

Aline Barreto de Moraes e Castro Philodemos,Eduardo Ferreira e Maria Beatriz Cardoso Nascimento

The Ministry of Environment (MMA), the Brazilian Institute of Environment and Renewable Natural Resources (Ibama), and Chico Mendes Institute for Biodiversity Conservation (ICMBio) regulated in January this year, by means of the joint normative rulings Nos. 1 and 3, direct and indirect modalities for conversion of environmental fines.

Provided for in the Federal Decree No. 6,514/08 (amended by Decrees No. 9,179/17 and No. 9,760/19), the conversion allows the agencies and entities that compose the National Environmental System (Sisnama) to convert simple environmental fines into services related to the preservation, improvement, and recovery of environmental quality, with the exception of fines arising from environmental violations that result in human deaths.

Although the new joint normative rulings do not change the procedure for the implementation of the conversion of environmental fines, they regulate some details that are relevant to the operation of the Fine Conversion Program.

Joint Normative Ruling No. 1, -responsible for regulating the direct modality of conversion of environmental fines, establishes that the defendant must implement by its own means the project for the provision of services related to the preservation, improvement and recovery of environmental quality. The Federal Environmental Public Administration will offer to the defendants the assessed project or project quota to be implemented, and may even indicate the adhesion to the indirect modality.

Projects submitted under the Administrative Procedure for Project Selection (PASP) or under a specific internal procedure, and approved by the institution responsible for organizing the selection, will only be part of the conversion projects portfolio after approval by the president of the agency or any other designated public agent . With such approval, the competent environmental authority will then indicate to the defendant the project which it considers to be compatible with the amount of the set fine.

In the direct modality, the defendant will be responsible for monitoring the environmental project and for bearing any related environmental costs. Implementation and monitoring reports must be periodically submitted to the competent environmental agency in order to verify the progress of project implementation and the achievement of the proposed results. After the request for direct conversion has been approved, the defendant must sign a commitment term in which will be established the conditions to be met.

Regulated by Joint Normative Ruling No. 3, the indirect modality of conversion of environmental fines provides, in its turn, that the defendant must contribute to the Environmental Fine Conversion Fund (FCMA) with the amount resulting from the fine, after application of the discount. The contribution will be allocated to cover the costs for the provision of services related to the preservation, improvement, and recovery of environmental quality. The defendant, in this case, is not directly involved in the implementation of environment’s beneficial measures.

When requesting the indirect conversion of environmental fines, the defendant must sign two different documents. The first is a commitment term, undertaking to pay to the FCMA the amounts involved in the conversion of the fine. The contribution to the FCMA must follow schedules that will be individually established with the competent environmental agency. The defendant that chooses this type of conversion must also sign an Instrument of Adhesion to the Fine Conversion (TACM), which will establish the conditions for the fulfillment of its obligations, with no responsibilities related to the monitoring or execution of the project.

As set forth in the two joint normative rulings, the conversion of environmental fines may be requested at three different moments, regardless of the chosen modality: (i) to the Environmental Conciliation Center, by the time of the environmental conciliation hearing, in which case a discount of 60% from the consolidated fine will be granted; (ii) to the judging authority, until the first instance decision, in which case a discount of 50% from the consolidated fine will be granted; and (iii) to the higher authority, until the judgment of the appeal, in which case a discount of 40% from the consolidated fine will be granted. Thus, the discount will not be based on the conversion arrangement chosen, but on the time when interest in conversion is expressed.

Another relevant aspect regulated by the joint normative rulings relates to the updating of the time frame provided for in Decree No. 10,198/20, published on January 3. The Decree postponed the date for the defendants who have already pleaded the conversion under Decree No. 9,179/17 to (i) withdraw the request submitted; or (ii) to submit a petition requesting the adjustment of its plea, in order to guarantee the application of a 60% discount from the amount of the consolidated fine (in this case, it will also be allowed to change the initially chosen modality of conversion of the environmental fine).

The original deadline was January 6, 2020, but it was extended to July 6. In case the defendant does not manifest an opinion on the new aspects of the regulation, tacit withdrawal of the request will occur. This will allow the authority that established the fine to continue with the environmental administrative proceeding.

The regulation on the conversion of environmental fines facilitates the resolution of administrative proceedings. However, notwithstanding the benefits herein indicated, it is important to remember that signing the respective commitment terms related to the conversion of environmental fines implies withdrawal of judicial and administrative challenges to the imposed fines and assumption of obligations that require time and investments.

- Category: Infrastructure and energy

After a broad process of regulatory review with public participation, the Brazilian National Electric Energy Agency (Aneel) identified the need to consolidate the rules regarding the obtaining of grants for alternative sources of power generation in order to simplify the procedures for submission, analysis of requirements, and management of grants.

As a result, on March 13, 2020, the agency published Normative Resolution No. 876/20, which established the requirements and procedures necessary to obtain authorization to operate wind, photovoltaic, thermoelectric, and other alternative power sources, including any request for changes in installed capacity. It also established rules for reporting the implementation of generating plants with reduced installed capacity for alternative non-hydraulic sources, such as wind, photovoltaic, and thermal power plants, among others.

On March 16, Aneel published another regulation, NR 875/20, which establishes the requirements and procedures necessary for (i) approval of hydroelectric inventory studies for hydrographic basins, (ii) obtaining authorization to operate hydroelectric power plants, (iii) reporting the implementation of hydroelectric power plants with reduced installed capacity, and (iv) approving technical and economic feasibility studies for hydroelectric power plants subject to concession.

In total, the new resolutions, in effect since April 1st, consolidate 11 normative resolutions in effect, standardizing rules, which until then were sparse, in accordance with Decree No. 10,139/19, and establish that all lower normative acts published by agencies and entities of the direct federal, instrumental, and foundational entities of the government must be reviewed in order to be consolidated.

In the case of NR 875, seven resolutions were unified concerning the preparation and approval of basic plans for Hydroelectric Power Plants (CGH), Small Hydroelectric Power Plants (SHP), and the use of hydraulic potential other than SHP, hydroelectric inventory studies, adjustment of deadlines for granting of SHPs, and granting of authorization for the use of hydraulic potential between 5 and 50 MW.

NR 876, in turn, has consolidated four normative acts that address the inclusion of the implementation schedule in authorizing acts and the granting of authorization for reduced capacity plants, wind power plants, and photovoltaic power plants.

In general, the new resolutions did not interfere with the merits of the normative acts consolidated, nor did they prejudice any potential subsequent improvements. The consolidation of the procedures was well received by players in the power sector, since the proceedings for obtaining and managing grants were simplified. The measure strengthens the legal and regulatory security of the Brazilian power sector and, consequently, favors the formation of a more secure and beneficial environment for business in the sector.

- Category: Institutional

In view of diverse legislative and regulatory changes published by governments in response to the COVID-19 crisis, we have teamed up with 11 law firms in Latin America and the Iberian Peninsula to prepare a table summing up the relevant changes that have occurred in Brazil, Spain, Portugal, Argentina, Bolivia, Chile, Colombia, Costa Rica, Ecuador, El Salvador, Guatemala, Honduras, Mexico, Nicaragua, Panama, Paraguay, Peru, Uruguay and Venezuela.

You can access the result of the work clicking here.

In addition to Machado Meyer, the participating law firms are: Aguilar Castillo Love (Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua and Panamá), BKM | Berkemeyer (Paraguay), Brigard Urrutia (Colombia), Cariola Díez Pérez-Cotapos (Chile), Ferrere Abogados (Bolivia), Guyer & Regules (Uruguay), Nicholson y Cano Abogados (Argentina), Quevedo & Ponce (Ecuador), Rodrigo, Elías & Medrano (Peru), Santamarina + Steta (Mexico), Torres Plaz y Araujo Abogados (Venezuela).

- Category: Infrastructure and energy

Alberto Faro and Felipe Baracat

Policies implemented by the federal government since 2016 have redesigned the role of the state in the infrastructure sector, focusing on private initiative as the main agent promoting the expansion of Brazilian infrastructure, both in the implementation and operation of these projects and in their financing.

In this context, the so-called infrastructure debentures or incentivized debentures, which enjoy the tax benefits created by Law No. 12,431/11, have played an important role in promoting the participation of private investments in the financing of the sector. They may be issued to finance projects that are part of the Investment Partnership Program (IPP) or that have been prioritized by the relevant ministries.

Since 2012, the average share of the capital market in the financing of the sector has not exceeded 10%, and it was only from mid 2016 that infrastructure debentures began to gain strength. According to information released by the Economic Policy Bureau of the Ministry of Economy, the issuance of infrastructure debentures reached R$ 23.9 billion in 2018, compared to only R$ 9.1 billion in 2017 and R$ 4.4 billion in 2016. In 2019, the total value of issues reached R$ 34 billion, an increase of 56% in relation to 2018; there were 98 issues, compared to 76 in 2018, with an average value of R$ 350 million.

Already consolidated as an important financing instrument in several other segments of the energy sector, incentivized debentures took time to advance in the case of the biofuels sector, largely because of the instabilities observed in the sugar energy industry in recent years. With the gradual resumption of new investments starting in 2016, however, and given the evolution of macroeconomic conditions since then, these instruments have become an attractive alternative for raising funds by players in the sector.

In this context, the Ministry of Mines and Energy (MME) updated the rules for approval of projects as priorities in the biofuels sector by issuing Ordinance No. 252/19, later amended by Ordinance No. 348/19. In addition to adjusting the regulations to reflect some updates introduced in Law No. 12,431/11 and Decree No. 8,874/16, the ministry also allowed projects aimed at implementing, expanding, maintaining, recovering, adapting, or modernizing the production and storage of biofuels and biomass to be classified as priorities for all purposes of Law No. 12,431/11.

The inclusion of a reference to biomass production and storage in the list of activities that may receive funds raised through incentivized debentures was particularly relevant in the case of the biofuels sector, allowing financing not only for the industrial stages of its production chain, but also production of the corresponding biomass. Another relevant changes concerns the possibility of classification of projects in which the production of biofuels is carried out at the same time as other non-energy products (such as sugar). In such cases, in order to define the amount eligible to raise funds through incentivized debentures, the proportion of biofuel production in relation to the total capacity of the project may be factored in, based on the industrial factors typical of that activity, according to technical parameters published by the Ministry of Agriculture, Livestock, and Supply.

Since then, the MME has already approved as priorities for the issuance of infrastructure debentures six projects in the biofuels sector, which include activities such as soil preparation, planting, sugarcane treatment, soil renewal, and loading and transportation of inputs, in addition to the implementation, maintenance, and expansion of industrial plants dedicated to the production of biofuels. Investments total R$ 9 billion in the sector.

Of the six projects in progress, we serve as legal counsel in three of them, which together exceed R$ 4 billion in expected funding in the capital markets. In this work, we support the issuing companies from the definition of the scope of the projects and their classification as priorities, including during the processing of the application at the MME, to the structuring of the financing transaction, including preparation, negotiation, and formalization of all documentation necessary for the issuance of the debentures.

In general, the documentation required for the classification is relatively simple, and the ministry has responded quickly. The team at the Bureau of Petroleum, Gas, and Biofuels, the body at the MME responsible for approving the classification of projects as priorities in the biofuels sector, has closely monitored these processes, standing out for its good relationship and technical cooperation with the market.

It appears that the new MME regulations represented an important step towards diversifying the sources of financing available for the biofuels sector. It is possible to observe a relevant growth in debenture issuances in the sector since September of 2019.

In addition to this change, there are other initiatives of the ministry on the radar, also directed at the biofuels sector and in the context of the National Biofuels Policy (RenovaBIO), such as the creation of a new financial security issued from the sale of biofuels, the Carbonization Credit (CBIO), which is already being traded on the B3.

Although this movement of sectoral innovations has been temporarily slowed down by the current pandemic, it is certain that the latest changes introduced by the MME for approval of projects as priorities, together with the other novelties, may reconfigure the sector's financing dynamics as soon as the uncertainties resulting from the current crisis are reduced.