- Category: Environmental

In response to the rupture of the Brumadinho dam (MG) on January 25th of this year, changes under study and already approved in the legislation aim to tighten the regulations of dams in Brazil. On June 25th, for example, the Chamber of Deputies approved three bills providing for specific regulations on environmental disasters caused by dams.

Bill No. 2,787/19 seeks to amend Federal Law No. 9,605/98, which deals with criminal and administrative environmental sanctions, in order to set forth the elements for the crime of ecocide (large-scale environmental destruction) and the criminal conduct of persons responsible for disaster relating to ruptures of dams in general. The bill also intends to increase the maximum fine for environmental administrative infractions from R$ 50 million to R$ 1 billion.

The second bill approved (2,791/19) is intended to significantly amend Federal Law No. 12,334/10, which established the National Dam Safety Policy, and seeks to prohibit the construction or elevation of mining by the upstream method and the implementation of mining dams whose rupture scenario studies identify communities in Self-Rescue Zones (ZAS). The bill also intends to create a specific administrative infraction for breach of the rule, with a fine that may vary from R$ 2 billion to R$ 1 billion.

The amendments aim to: (i) extend the obligations of entrepreneurs and provide for their liability not only for dam safety, but also for damages resulting from their rupture, leakage, or malfunction and, regardless of fault, for the repair of such damages; (ii) increase the obligations and requirements of the Dam Safety Plan and the Emergency Action Plan (PAE) - preparation of a PAE will be mandatory for all dams classified as medium and high risk or medium and high potential associated damage and for all those intended for the accumulation or final or temporary disposal of mining tailings; and (iii) allow the supervisory body to demand from entrepreneurs the presentation of a bond, insurance, surety, or other financial or real guarantees for the reparation of damages to human life, the environment, and public property.

If the bill is approved, supervisory agents will be required to set up a communications channel to receive complaints and information related to dam safety, and an accreditation system for individuals and legal entities that may certify dam safety.

Bill No. 2,788/19, in turn, establishes the National Policy for Persons Affected by Dams (PNAB), whose provisions apply to the environmental licensing of dams and to emergencies arising from the leakage or rupture of such a structure, whether already occurred or imminent. For the purposes of the future law, the text defines (i) dams as being those regulated by Law No. 12,334/10 and others that, by their construction, affect local populations; and (ii) affected populations as being those suffering at least one of the ten situations provided for, such as loss of possession or ownership of property, loss of productive capacity of the land, or alteration of water quality that impairs supply.

The text of the bill lists the rights of the population affected by dams, including: (i) reparation through compensation; (ii) collective resettlement; (iii) independent technical advice paid for by the entrepreneur to guide residents; (iv) emergency assistance in the event of accidents or disasters in order to ensure that living standards are maintained until families have recovered; (v) compensation for individual and collective moral damages; and (vi) equivalent housing for those in the affected area. In addition, the bill intends to remove from the Consolidated Labor Laws (CLT) a provision that limits compensation to workers for moral damages arising from the labor relationship.

Entrepreneurs will also be required to finance and implement the Program for the Rights of Populations Affected by Dams (PDPAB), which aims to ensure the rights established in the PNAB. A national consultative and deliberative board will be responsible for monitoring, overseeing, and evaluating the formulation and implementation of the PNAB.

The three bills followed for consideration by the Federal Senate. Their approval in the Chamber of Deputies demonstrates the intense action of the Brumadinho External Disaster Commission, formed to monitor and inspect the existing dams in Brazil and the investigations related to the disaster that struck the municipality in Minas Gerais. At least three other bills are still pending approval by the Chamber of Deputies.

- Category: Labor and employment

Trade union dues were created in the 1940s in order to strengthen the trade union movement. This was a mandatory amount due from the worker to the professional trade union of his category, even if he were not affiliated to it, and corresponded to the remuneration of a normal work day.

This compulsory system had already been criticized by the majority of legal scholarship, according to which application of the freedom of association and the autonomy of trade unions required a change in the method of collecting trade union dues in order to make them voluntary and to encourage positive union actions on the part of trade unions vis-à-vis their category.

Law No. 13,467/17 (the Labor Reform) eliminated the obligatory nature of the dues, whose collection is now subject to prior and express authorization by the worker, pursuant to article 579 of the Consolidated Labor Laws (CLT). However, some gaps in the amended text of the CLT have generated room for different interpretations regarding the need for the worker’s authorization to deduct the dues: a first current believes that the authorization must be individual, given exclusively by the worker himself; the second current believes that the union may convene a general meeting to vote to authorize the discount relating to the dues of its affiliated workers; and the last current believes that the trade union may convene a general meeting to vote on the authorization of the discount related to the trade union dues of the workers of the category it represents, valid even for those not affiliated with the entity.

Some trade unions took advantage of possible interpretations of the law, as well as the principle of prevalence of what is negotiated over what is legislated (also implemented by the Labor Reform) to negotiate conditions with employers that would allow for the compulsory discounting of dues, which was seen by the Ministry of Economy as affront to the Labor Reform.

To put an end to the controversies, on March 1st the federal government promulgated Executive Order No. 873/19, also known as the Trade Union Contribution MP, with the main purpose of stipulating the mandatory individual authorization of workers and payment via bank slip. This would eliminate the possibility for trade unions to obtain authorization for compulsory discounting via a general meeting.

Because it was not converted into law within the period established in the Federal Constitution, MP 873/19 lost its effectiveness, on June 28. The original text of the Labor Reform on the subject thus again entered into force, bringing in legal instability on the issue.

Despite this situation, the Federal Supreme Court (STF) has established an understanding similar to the one stipulated by the executive order, that is, that authorization to discount trade union dues must be provided individually by the worker.

On June 28, Justice Luis Roberto Barroso granted an injunction in the record of Case No. 35.540, suspending an order by the 48th Labor Court of Rio de Janeiro for the company Claro to deduct trade union dues from the payroll of its employees, regardless of prior individual authorization, on the understanding that the charge may be authorized by a general meeting of the category.

In granting the injunction sought by Claro in the labor claim filed, Justice Barroso stressed that the Federal Supreme Court had already decided in the judgment of Direct Action of Unconstitutionality No. 5.794 that the provisions of the Labor Reform that establish the end of compulsory dues were constitutional. The Justice stressed that the power of general meetings to approve the collection of trade union dues is inconsistent with the new regime and interpreted that, under the law, prior and express authorization by workers is mandatory and cannot be replaced by the will of the general meeting of the category.

Although not classified by the STF as being a topic with general repercussion, the decision is a further guideline for companies regarding the STF's tendency in interpreting the matter, which, for the moment, is in line with the terms of MP 873/19, now no longer in force.

- Category: Banking, insurance and finance

Law No. 12,414/11, as amended and regulated by Decree No. 9,936/19, regulated the formation and consultation of databases with information on performance, mandating, in its article 12, paragraph 3, that the National Monetary Council (CMN) adopt complementary measures and standards on the provision of information by institutions authorized to operate by the Central Bank of Brazil (BC).

In this sense, CMN Resolution No. 4,737, issued on July 29, addresses the following topics:

- the provision of information to database managers registered by the BC;

- the obtainment of and the scenarios for cancellation of the registration as database managers in the BC; and

- the designation and qualifications required for the positions of officer responsible for database management and officer responsible for information security policy.

Provision of information. With respect to item “a” above, the resolution requires financial institutions and other institutions authorized to operate by the BC to provide registered database managers with the information that makes up the history of transactions conducted with their customers, including: (i) credit transactions; (ii) leasing transactions; (iii) self-financing transactions through consortium groups; and (iv) other transactions with characteristics of credit extension.

For the purposes of the new standard, information on the history of a particular transaction, as well as on amounts involved, form of payment, and installments paid by the customer is considered.

The provision of data on the transactions performed does not imply breach of the bank secrecy provided for in Complementary Law No. 105/01, provided that the (registered) customer has expressly requested its inclusion to the database manager. It is important to highlight that both financial institutions and other institutions authorized to operate by the BC and database managers must comply with the provisions of Law No. 13,709/18, as amended (General Personal Data Protection Law), concerning the parameters applicable to the use of personal data.

The standard also establishes that, upon transfer or sale of a transaction, the institution responsible for providing the data is the one that keeps the accounting record of the transaction among its assets, as provided for in current regulations.

Registration of managers and qualifications required. Resolution No. 4,737/19 defines the requirements for database managers to obtain a registration with the BC, including the designation of the officer responsible for database management and the officer responsible for information security policy. They will hold their positions for a maximum term of four years, renewable for equal periods.

Officers must meet a number of requirements under the new resolution for them to be able to perform their duties, including, but not limited to: (i) having an unblemished reputation; (ii) not being prevented by special law, or convicted of a bankruptcy crime, tax evasion, malfeasance, active and passive corruption, graft, embezzlement, crimes against the popular economy, the public faith, property, or the National Financial System, or sentenced to criminal punishment that prohibits, even temporarily, access to public office; (iii) not being declared unqualified for or suspended from the exercise of the positions of audit committee member, member of the board of directors, executive officer, or managing partner in financial institutions and other institutions authorized to operate by the BC; and (iv) not being declared bankrupt or insolvent.

Both officers must also have technical qualifications commensurate with the duties of their positions, proven on the basis of academic background, professional experience, or technical knowledge specific to their occupations.

The conditions listed above shall also be observed by members of controlling groups, in the case of a database manager organized as a corporation or limited liability company, except for managers controlled exclusively by institutions authorized to operate by the BC. For the purposes of the CMN's resolution, a controlling group is a group that holds partner rights corresponding to the majority of the voting capital of a corporation or 75% of the capital stock of a limited liability company.

Registration of database managers may be rejected by the BC if circumstances that affect the reputation of the members of the controlling group and/or the officers appointed are found. Another scenario for rejection is omission or provision of documents, data, or information that is incorrect or in disagreement with the applicable standards, considering the circumstances of each specific case and the public interest.

Resolution No. 4,737/19 also provides for situations for cancellation of the registration of database managers, which may occur in the event of: (i) non-compliance with the conditions set forth in the standard in question; (ii) omission or provision of documents, data, or information that is incorrect or in violation of legal or regulatory standards; or (iii) absence of appointment of a substitute for the duties of officer responsible for database management or a officer responsible for information security policy, 45 days after the discharge of an officer responsible for these functions. In all cases, database managers will be given a deadline to respond to the cancellation of their registration.

- Category: Corporate

The modernization of disclosure of company information has finally gained momentum in Brazil. Published on August 5, Executive Order (MP) No. 892/2019 substantially changed the framework for legal publications by corporations.

This is a subject that has been much discussed over the last few years, especially because of the exponential evolution of the internet and the means of access to information on companies currently used by their shareholders and the market in general.

While companies are eager to reduce their costs with publishing in newspapers, which in reality no longer fulfill the purpose of disseminating information to the market, printed media, which charge considerable amounts for the service, insist that the dissemination of information in newspapers still has a purpose.

The fact is that MP 892 extinguishes the need to publish, both in the official gazettes and in printed newspapers published in the locality of company headquarters, of all acts whose publication is mandated by Law No. 6,404/1976 (the Brazilian Corporations Law). The measure also establishes that, based on the regulations of the Brazilian Securities and Exchange Commission (CVM), in the case of publicly-held companies, and per the Minister of State, in the case of privately-held companies, legal publications are made exclusively on the websites of the CVM and the market management entities on which securities issued by the companies are admitted for trading.

In practice, MP 892 simplifies the administrative and corporate routine of companies, especially publicly-held companies, generating savings and faster disclosure of relevant information to the market in general. MP 892 also states that digital publications mandated by it may not be charged fees by the CVM and/or B3.

The measure updates a norm from the 1970s to conform with the current reality and seems to us to be beneficial to the Brazilian market in every respect. However, special attention needs to be paid to the effectiveness of MP 892, as the definitive implementation of the purely digital publishing system still needs regulations. The text states in its article 5 that only on the first day of the month following the issuance of the regulations shall the changes promoted take effect.

MP 892 will be effective for a maximum of 60 days, renewable for the same period, and will lose its validity if not converted into law by the Brazilian Congress. Statements by the Speaker of the Chamber of Deputies in reaction to the publication of MP 892 suggest that there may be adjustments and a transitional regime may be proposed.

Accordingly, until the regulations are issued, the old rules that require publication in the newspapers for various acts of companies, such as corporate reorganization, issuance of securities, and convening of shareholders' meetings, will still be in force. Failure to comply with the old rules may lead to administrative and judicial litigation regarding the validity of the acts in question.

Although the CVM’s regulation on the publication of relevant information is already considerably aligned with the objective of MP 892, it is necessary to await the new regulations in order to be able to evaluate what the impacts will be for publicly-held companies’ disclosure policies and the receptivity of the market to the new regime.

Depending on the rules established, MP 892, if converted into law, has the potential to encourage increase in the number of corporations in industries in which this type of company has never predominated precisely due to the existence of higher additional costs.

- Category: Labor and employment

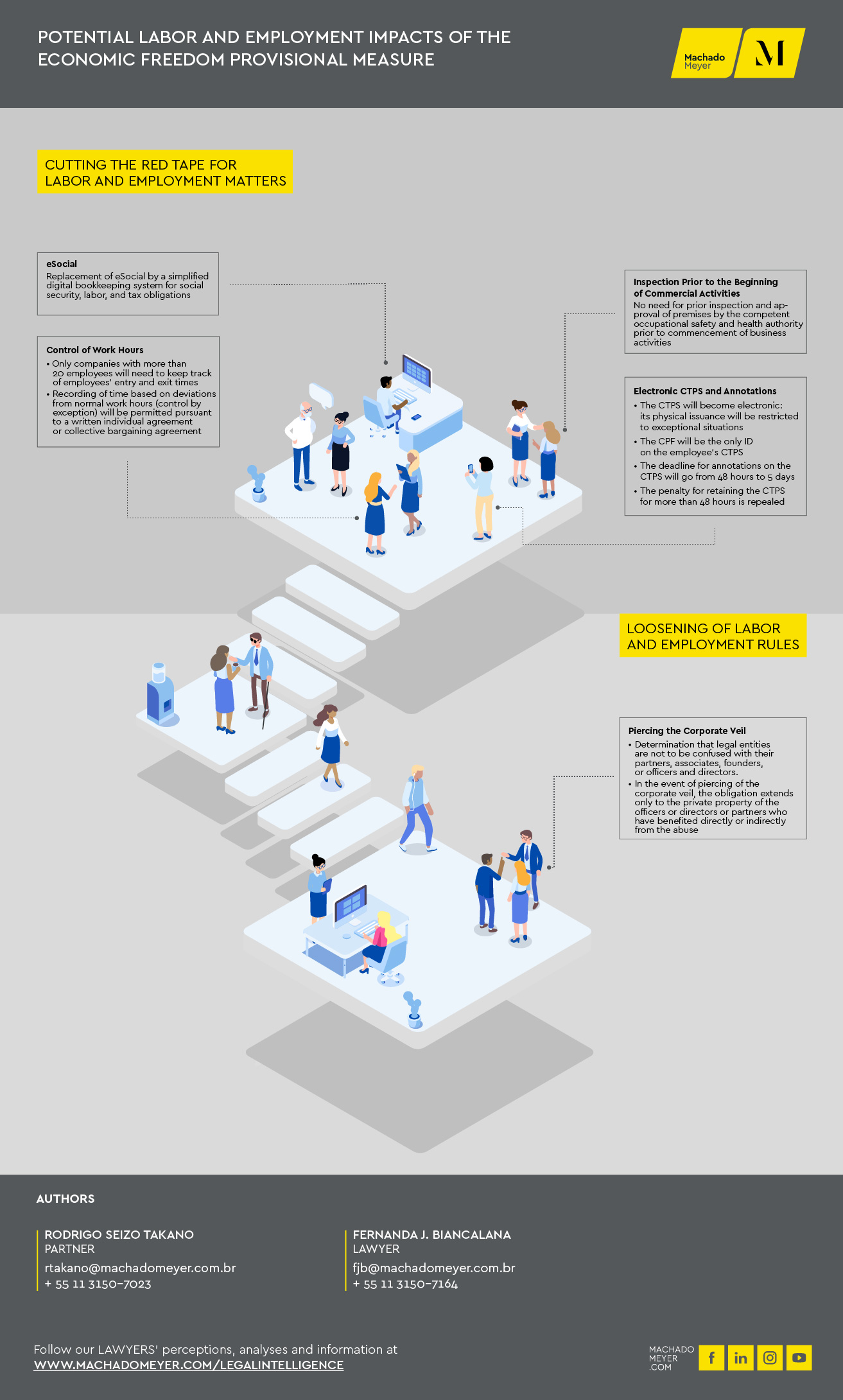

The publication of Ordinance No. 604/19 of the Special Secretariat of Welfare and Labor, which deals with work on Sundays and holidays, from a practical point of view, brought in important impacts to various sectors, especially trade and tourism.

One of the main changes for employers is permanent authorization for work on Sundays and holidays, with the elimination of the obligation for collective bargaining or administrative requests to the competent authorities for this purpose.

Compared with the ordinance previously in force, the number of categories (from 72 to 78) authorized to work on Sundays and holidays was expanded, including new economic sectors: the vegetable oil and biodiesel extraction industry, the wine and grape derivatives industry, the aerospace industry, commerce in general, tourism establishments, and aerospace maintenance services.

All activities for which work on Sundays and holidays has been authorized are identified in the schedule attached to the ordinance. Except for some specific sectors, office jobs are excepted.

Companies legally authorized to operate on these days, regardless of the economic sector in which they operate, must organize shift schedules, ensuring that workers enjoy time off on certain Sundays, within the legal norms.

When work occurs on Sundays or public holidays, employees shall be entitled to compensatory weekly rest on any other day within the same week, and there is no need to remunerate such work as overtime. However, if the compensatory break is not granted in the same week, that day must be paid double.

As article 6 of Law No. 10,101/2000 has thus far not been repealed, there will be discussions regarding whether or not there is a need for municipal legislation authorizing the activities of commerce in general on Sundays.

All discussion regarding work on Sundays and holidays for categories not covered by Ordinance No. 604/19 may be near the end. The Joint Committee set up to review the bill to convert Provisional Measure (MP) No. 881/19 into law, known as the Economic Freedom MP, on July 11 approved the opinion of Deputy Jeronimo Goergen (Progressive Party) that article 68 of the Consolidated Labor Laws (CLT) should be amended. With the change, all categories are authorized to work on Sundays and holidays, with paid weekly rest guaranteed on Sundays once every four weeks of work, which should end potential debates on the subject.

However, the bill regulating the MP still needs to go through the House and Senate en banc before being submitted for signature by the President of Brazil. Only if the text is approved as it was drafted, will work on Sundays and holidays be guaranteed for all categories.

The current government has shown its intent to stimulate the country's economy through changes in regulations to create opportunities for consumption and, most likely, jobs. It also demonstrates that it is trying to fulfill its promise to reduce red tape regarding labor relations made during the election campaign.

This type of regulation brings about security in labor relations and creates more opportunities for production and consumption. There is a clear need for various sectors to operate on Sundays and holidays, which makes it absolutely necessary to disentangle the operation of business establishments, with the removal of numerous rules regarding work on these days.

- Category: Labor and employment

Resolution No. 241 of the Superior Council of the Labor Judiciary (CSJT), in force since June 6, amends some of the rules of Resolution No. 185, bringing in important changes in the use of the Electronic Judicial Procedure (PJe).

For the practice of labor law, there are some changes, such as the possibility of submitting an answer, counterclaim, and documents accompanying them under seal, without the magistrate being able to order them excluded, and the obligation to use the PJe-Calc tool to submit calculations of judgment debt.

The changes were provided for by law, respectively, in paragraphs 4 and 6 of article 22 of the new resolution. In the past, it was possible to file an answer, counterclaim, and documents in a confidential manner, provided that the parties supported the confidentiality based on the scenarios set forth in article 770, head paragraph, of the CLT (Consolidated Labor Laws) and articles 189 or 773 of the CPC (Code of Civil Procedure).

The first opportunity in positive law to file the briefs in question under seal arose with Resolution No. 94/13 of the same council. However, the change made by Resolution No. 185 created a paradox: either the documents were filed without confidentiality, exposing the theory in defense before the hearing, which changes the practice observed at the time of physical proceedings and relativizes the provision of article 847, head paragraph, of the CLT, or the briefs were presented under seal, delivering them for the subjective review of the magistrate.

In this subjectivity, of course, there are appellate decisions that modify the striking of documents ordered by trial judges and also those that uphold them.

Setting aside the decision by the trial court that ordered the striking of the answer and documents presented by the company, the judgment handed down in the record of case No. 0000622-18.2018.5.21.0009, of the authorship of appellate judge Ronaldo Medeiros de Souza, of the 2nd Panel of the Court of Appeals for the 21st Circuit, addressed in detail the topic of confidentiality:

"Law No. 11,419/2006, which provides for the computerization of judicial proceedings, promoted a radical change in the way the procedural acts are performed, so that, today, we are improving the electronic mechanisms and changing the procedural legislation order to ensure greater compatibility between the two.

However, it is the PJe-JT System and its peculiar rules that are subject to labor procedural legislation, not the other way around. In this sense, article 847, head paragraph, of the CLT indicates that the opportune time for the presentation of the answer in a labor claim is after the first attempt at settlement has been frustrated, being an option of the party, to do so orally or, per the terms of the sole Paragraph of the legal provision in question, to present it in writing via the electronic judicial proceeding system before the hearing.

As the respondent has pointed out well, the fact that it submits its defense in advance through the PJe-JT System does not imply that the opposing party must have access to it before the appropriate procedural moment, i.e., after the first attempt at settlement. The logic that presides over this system is, as the respondent said, to "foster and preserve good dialogue in negotiation, delaying the adversarial nature of the process" (675).

Interestingly, the same court has a decision in the entirely opposite direction, ratifying the exclusion of the answer and its documents, as seen in the headnotes below:

HEADNOTES

Answer. Confidential nature. Non-receipt. Curtailment of defense. Nullity cured. Absence of prejudice. Ripe Cause. Decision on the request. The filing of the answer under seal does not impose an obstacle on the Court blocking its review, still more so when the time limit set by it for it to be presented is observed. Moreover, the scenario at bar does not challenge the application of the provisions of paragraph 2, of article 9, of TRT21 Act No. 634/2013, since, at the time of the filing of said briefs, the first hearing had not yet taken place. However, even rejecting the answer, the trial court did not declare default, and validated all the evidence submitted by the defendant, in addition to, during the course of the pre-trial phase, granting it full exercise of the right of defense, such that the suit was duly instructed, in such a manner that it is not possible to declare the nullity, due to application of the provisions set forth in article 794 and 796, a, of the CLT. (TRT-21 - ROPS: 00002731520185210009, Date of Decision: November 6, 2018, Date of Publication: November 9, 2018. Opinion drafted by: Ricardo Luís Espíndola Borges)

Thus, Resolution No. 241 of the CSJT comes in good time to end the debate regarding the use of the “confidentiality" option in filing the answer, counterclaim, and documents. The magistrates are expected to accept the content of the resolution, which, we should agree, did nothing more than ensure compliance with the head paragraph of article 847 of the CLT for lawsuits proceeding via electronic means.

The other important novelty brought about by Resolution No. 241 of the CSJT was the mandatory use of PJe-Calc, a tool developed to standardize the presentation of calculations in labor suits. This is a very complete solution that, although considered "didactic" and "intuitive" by its creators, has a complex instruction manual and several videos explaining its operation. Perhaps for this reason compulsory use was delayed until January of 2020.

Resolution No. 241 of the CSJT, therefore, brings the PJe closer to the labor practice, making technology work for the practice of law, and not vice versa, as it is not uncommon to find situations where practices affecting physical proceedings are hampered by the characteristics and functionalities of the electronic procedure.

Keywords:

- Category: Tax

For some time the classification of ICMS tax incentives as an investment subsidy has long been debated in the tax courts. The relevance of this discussion stems from the possibility of excluding income from investment subsidies from the IRPJ (Corporate Income Tax) and CSLL (Social Contribution on Net Income) calculation bases.

The Federal Revenue Service of Brazil (RFB) often questions exclusions of this nature on the grounds that, in fact, these are revenues from funding subsidies. The questions suffered by taxpayers are as varied as possible, such as: failure to invest funds from the subsidy in the projects incentivized, lack of synchronization between the amounts invested in the projects and recognition of revenues from subsidies, improper classification of presumed ICMS credit benefits as investment subsidies, and limitation on the exclusion of revenues from investment subsidies up to the values of the projects subsidized.

With the promulgation of Complementary Law No. 160/2017 (LC 160/2017), the legislator provided that ICMS incentives must be considered investment subsidies for the purposes of the IRPJ and CSLL and forbade mandating any other requirements not provided for in article 30 of Law No. 12,973/14.

Through LC 160/17, the legislator also provided that the above treatment applies also to administrative and judicial proceedings not yet definitively adjudicated, as well as to ICMS incentives granted in disagreement with the constitutional requirements. In the latter case, the law required the granting states to register and deposit their respective normative acts with Confaz (the National Council for Finance Policy), following the solution proposed for the context of the “tax war.”

At the same time, on recent occasions, the Superior Court of Appeals (STJ) has reviewed the application of the IRPJ and CSLL on income arising from ICMS incentives. On these occasions, the Court approached the discussion in a manner that was quite broad and dissociated from the provisions of LC 160/17 on the subject. In this context, the First Section of the STJ found that the benefits granted by the states of the Federation in the form of presumed ICMS credits should not be subject to application of the IRPJ or CSLL, under penalty of offense to legal certainty, the federative pact, and reciprocal immunity (article 18 and 150, VI, “a”, of the Federal Constitution).[1] In the STJ's view, taxation of these amounts by the Federal Government would have an impact on the benefit granted by the state (Motion to Resolve Divergence in Special Appeal 1.517.492-PR).

As may be seen from the deciding vote cast in that judgment, presumed ICMS credits cannot be considered corporate profit, as they correspond to waiver of revenue by the state government, which acts within its competence and in accordance with its tax policy. Thus, it is fitting for the Federal Government to tax such amounts, since it would "obliquely withdraw the tax incentive which the Member State, in the exercise of its tax competence, granted."

It is important to highlight that this judgment does not address the classification of tax benefits as an “investment subsidy”, nor does it address any requirements established by article 30 of Law No. 12,973/14.

Subsequently, the STJ was urged to rule on the maintenance or modification of the position adopted in EREsp 1.517.492/PR, in view of the supervening enactment of LC 160/2017. At all times, the Court found that it was not the appropriate time to review the effects of LC 160/2017, as the law came into force after the National Treasury filed special appeals and it had not been challenged by the local court (issue not previously raised). In any case, the decisions expressly state that the entry into force of LC 160/2017 would not be able to change the position established in EREsp No. 1.517.492-PR regarding the violation of the federative pact.[2]

Admittedly, this position should not be considered definitive, since the provisions of LC 160/2017 on the subject have not yet been specifically analyzed by the STJ en banc, which should occur shortly. In addition, the guiding basis for the STJ's decision on the merits is constitutional in nature. In principle, the last word on the matter should be the responsibility of the STF (Federal Supreme Court), which may review the decisions in question in the context of an Extraordinary Appeal.

The STF itself has previously recognized the general repercussion regarding the taxation of presumed ICMS credits for PIS and Cofins (RE No. 835 818-PR), which, although dealing with different taxes, has as one of its arguments precisely the offense to the federative principle and the interference of the Federal Government in the exercise of the competence of a state tax.

In summary, based on the recent precedents of the STJ that the Federal Government cannot tax benefits granted by states, as this represents an affront to legal certainty, the federative pact, and reciprocal immunity, it is possible to discuss the need regarding whether or not to observe the requirements established by article 30 of Law No. 12,973/14. Among them, the most relevant for taxpayers is the obligation to allocate income from subsidies in a tax incentive reserve account, i.e., a profit reserve.

From the STJ's position on the subject, even without settling the controversy, it may be inferred that there are legal arguments to support the possibility of excluding the subsidized amounts from the IRPJ and CSLL calculation bases, despite the accounting of these amounts in a profit reserve.

[1] Article 18. The political and administrative organization of Federative Republic of Brazil includes the Federal Government, the States, the Federal District, and the Municipalities, all autonomous, per the terms of this Constitution. (...).

Article 150. Without prejudice to other guarantees provided to taxpayers, the Federal Government, the States, the Federal District, and the Municipalities are prohibited from: (...) VI - instituting taxes on:

- a) property, income, or services from one to the other; (...)

[2] In this sense: Interlocutory Appeal in Special Appeal No. 1.306.878-RS; Interlocutory Appeal in Special Appeal No. 1.726.562-RS; Interlocutory Appeal in Motion to Resolve Divergence in Special Appeal 1.462.237-SC; Interlocutory Appeal in Special Appeal No. 1.794.524-PR; Interlocutory Appeal in Special Appeal No. 1.725.131-SC; Interlocutory Appeal in Special Appeal No. 1.729.965-SC; Interlocutory Appeal in Special Appeal No. 1.675.331-PR.

- Category: Corporate

Presidential Decree (MP) No. 881, published on April 30 of this year, instituted the Declaration of Economic Freedom Rights and amended a series of legal provisions of a corporate, civil, real estate, and tax nature.

In this article, we shall analyze the main provisions of the MP, classified according to their nature.

Corporate

The provision that most attracted attention from the corporate point of view was the inclusion of a sole paragraph into article 1,052 of the Civil Code that authorizes the formation of limited liability companies by only one partner. The requirement to have at least two partners to form a limited liability company is an old discussion that culminated in 2011 in the establishment of the Individual Limited Liability Company (Eireli). Even though it may be formed by only one owner, the Eireli did not fully meet the expectations of the business world.

In order to comply with the provisions of the MP, the National Department of Business Registration and Integration (Drei) issued Normative Instruction No. 63, published in the Official Federal Gazette on June 14, to deal with the registration requirements and procedures for the individually owned limited liability companies. According to the rule, this type of company may originate from an original incorporation, departure of partners from the company by means of an amendment to the articles of association, as well as transformation, merger, spin-off, etc. The instruction also establishes that all the rules pertaining to limited liability companies organized by two or more partners must apply to individually owned limited liability companies.

The presidential decree also amended the provisions of the Civil Code dealing with Eirelis so as to make it clear that, except for cases of fraud, only an Eireli's assets are used to satisfy the company's debts, but they are not to be mixed in any situation with the assets of the owner of the Eireli.

Also in the context of personal liability, the Presidential Decree officialized the institute of inverse piercing the corporate veil by including a new paragraph in article 50 of the Civil Code to deal expressly with the subject. That is, the obligations of partners or managers may be extended to the legal entity is cases of abuse characterized by misuse of purpose or intermingling of assets.

In addition to defining what misuse of purpose and intermingling of assets is, the MP introduced into the Civil Code, in a clear manner, a provision according to which, in cases of abuse, the judge may effectively pierce the corporate veil. Previously, article 50 dealt in a more generic manner with the extension of the effects of certain relationships of obligations with the private assets of partners and managers, without expressly mentioning piercing the corporate veil per se.

Article 50 also provided in paragraph 4 that the mere existence of an economic group does not lead to piercing of the corporate veil. The insertion is important, since it seeks to increase the legal certainty of companies that are part of economic groups, sometimes held liable due to the simple fact that they are part of the same group and without due observance of the legal requirements for piercing the veil.

The requirements of the MP to give rise to piercing of the corporate veil should be considered, as regards real estate issues, when acquiring real estate belonging to specific purpose entities or companies that, in general, may be part of economic groups in situation of crisis or debt restructuring, but which in themselves do not pose a risk to the acquirer.

The latest change to the Civil Code of a corporate nature relates to the inclusion of provisions that define the investment fund, delegating to the Brazilian Securities Commission (CVM) the responsibility for disciplining it, but establishing that such a fund may, observing the rules issued by the CVM: (i) establish the limitation of liability of each condominium to the value of its units/quotas; and (ii) authorize the limitation of liability of fiduciary service providers vis-à-vis the condominium and among them, to the fulfillment of the particular duties of each one of them, without joint and several liability. If a fund established without limitation of liability wishes to adopt limited liability, this limitation will only cover the facts that occurred after this change.

With regard to the Brazilian Corporations Law, the MP brought in two novelties. The first of these is the possibility for the CVM to issue regulations that waive certain requirements set forth in the same law for companies that it defines as small and medium-sized, in order to encourage and facilitate the access of these companies to the capital markets. The second innovation consists of dispensing with the signature of shareholders subscribing shares on the subscription list or form, in the event of a public offering, the settlement of which occurs through systems managed by entities managing the organized securities markets.

Civil

The MP also amended the articles of the Civil Code dealing with contracts in general so as to provide that, in addition to the freedom to contract within the limits of the social function of contracts, the provisions of the Declaration of Economic Freedom Rights and minimum intervention by the State in private contractual relations must also be observed.

The provisions of the Civil Code on adhesion contracts have also been amended. The old wording provided that, in cases of ambiguous or contradictory provisions in adhesion contracts, construction should done in the manner more favorable to the adherent (i.e., the party who did not draft the contract). The new wording only changed "ambiguous or contradictory" to "that cause doubt regarding construction." In addition, it was established that the same logic should apply to non-adhesion contracts, but in which one of the parties did not draft the provision. That is, in contracts, even if they are not adhesion contracts, the provisions should be construed for the benefit of those who did not draft them, in the event of doubts.

Also in the civil sphere, the MP amended Law No. 11,101/05, which governs judicial reorganization, including a new article 82-A, which deals with the extent of the effects of bankruptcy. This inclusion, in and of itself, is questionable, since this law already has other mechanisms for third-party liability in the event of bankruptcy.

Moreover, although extension of the effects of bankruptcy had already been applied and accepted by a significant portion of the Brazilian courts, there was no legal provision governing it, which ultimately created uncertainty regarding the effects of such a measure (for example, on the time limit to be fixed for the companies/persons affected by the extension).

By introducing the institute through the presidential decree, the legislator has apparently attempted to mitigate lessen uncertainty and ensure some predictability regarding its use. As per the provisions of article 82-A, however, the attempt may not yield the fruit desired. Due to the seriousness of the alternative that the legislator has opted for, detailed regulations on its requirements (which should not be exactly the same as those for piercing of the corporate veil, as proposed), limits of application, effects, and extension would be recommendable, which is not seen in the text of the MP.

In order to reduce the bureaucracy related to the printing and storage of physical documents and to preserve the environment, the MP also changed the wording of Federal Law No. 6,015/1973 in order to permit the preparation and storage of public records in digital media, giving them the same validity as physical documents for all legal purposes.

Likewise, Federal Law No. 12,682/2012, which regulates the preparation and archiving of public and private documents on electromagnetic media, was also amended.

Real Estate

Another provision brought in by MP 881 concerns the amendment of Decree-Law No. 9,760/46, which deals with properties owned by the federal government, including naval lands. The new text alters the jurisdiction to hear appeals relating to decisions on demarcation of naval lands.

The task was assigned to the Minister of Planning, Budget, and Management, but was transferred, with the new norm, to the hierarchical superior of the secretary of Coordination and Governance of the Assets of the Federal Government of the Special Secretariat of Privatization and Divestment of the Ministry of Economy. In general, the change may accelerate the response to appeals filed by parties interested in proceedings before the Secretariat of Assets of the Federal Government (SPU).

Tax

Among the changes promoted by the presidential decree in the tax area, one may highlight the following points:

- Creation of a committee composed of members of the Administrative Council of Tax Appeals, the Special Secretariat of the Federal Revenue of the Ministry of Economy, and the National Treasury Attorney-General to promulgate restatements of law by the federal tax administration (article 14 of the MP - inclusion of article 18-A into Law No. 10,522/2002).

In the article in question, the restatements must be observed in the administrative, regulatory, and decision-making acts of said bodies, which are under the Federal Public Tax Administration.

- Expansion of the scenarios provided for in article 19 of Law No. 10,522/2002, in which the Attorney-General of the National Treasury (PGFN) will be exempt from answering, offering counter-arguments, and appealing or withdrawing from appeals (article 14 of the MP).

Among the scenarios provided for are the topics judged on the basis of concentrated and diffuse control of constitutionality, as well as repetitive appeals reviewed by the Federal Supreme Court (STF) and the Superior Court of Appeals (STJ), in addition to the provisions in binding precedents. This provision is in line with the new provisions of the Code of Civil Procedure of 2015, which seeks procedural speed and economy through the standardization of case law understandings.

MP 881 also ended up bringing in as a scenario for exemption from challenging/appealing the issues decided by the STF, the STJ, or by the Panel for Uniformization of Case Law (an integral part of the Federal Justice Council) when there is no possibility of reversing the theory settled in a sense unfavorable to the National Treasury, according to criteria defined in the act of the attorney-general of the National Treasury.

Likewise, the possibility of exemption of the PGFN from contesting/appealing was inserted in relation to cases that are the subject of a precedent of the federal tax administration, provided for in article 18-A, discussed above.

- Change and inclusion of specific procedures for exemption from establishment of a tax liability and collection by the Public Administration in the cases of exemption dealt with in article 19 of Law No. 10,522/2002 (article 14 of the MP - amendments and inclusions promoted in articles 19, 19-A, 19-B, 19-C, and 19-D of Law No. 10,522/2002).

Rights of economic freedom

In addition to amending legislation, MP 881 established the rights of economic freedom, assigned to every person, whether an individual or legal entity, and considered essential for Brazil's economic growth and development, two of which we highlight.

The first is the right of any person, whether an individual or legal entity, to develop a low-risk activity, for one’s own sustenance or that of one’s family, on private property or that of consenting third parties, without the need for licenses, authorizations, registration, and other acts that are required by public agencies before the exercise of the economic activity.

The Ministry of Economy published Resolution No. 51/2019, which defines the concept of low risk for the purposes of exemption from the requirement of public acts for release for operation or functioning of an economic activity. Examples of low-risk activities include news agencies, psychology, language instruction, tire installation services, etc. In such cases, supervision of the exercise of this right shall be carried out ex post facto, ex officio, or as a result of a complaint by a third party.

From the point of view of real estate law, it is possible that certain activities may be exempted from municipal licenses for installation and operation in order for them to operate.

The other right that we highlight is that the private party requesting a license, authorization, registration, enrollment, permit, or other acts required as a precondition for the exercise of an economic activity (upon presentation of all documents and elements necessary to support the process) shall be informed immediately regarding the maximum time limit for examination of the respective application.

After such period has elapsed without the authority having responded, the request shall be deemed tacitly approved, except for those cases expressly prohibited by law and when the request has been made by a public agent or relatives at certain levels of the administrative authority of the body itself in which the activities are carried out. MP 881, however, makes exceptions for cases in which such right will not be applicable, as in relation to tax matters and situations considered to have justifiable risk.

It should be noted that the entrance into force of the right to guarantee reasonable time limits is suspended for 60 days as of the date of publication of the presidential decree.

A review of the main changes made allows one to conclude that MP 881 may stimulate entrepreneurship in Brazil through the establishment of more flexible rules for certain types of business, but many of the new provisions depend on future and specific regulations for their effectiveness to be ensured.

Currently in progress before the National Congress, the text needs to be converted into law within 60 days (extendable once for an equal period) in order not to lose its effectiveness.

- Category: Infrastructure and energy

Now that the euphoria with the result of the 5th Round of Airport Concessions has passed, an analysis of the results obtained reveals a maturation of the concessions model adopted by the federal government. Choices made in the past, however, still pose challenges for the most varied of players in the industry, both in the public and private spheres. The proposal to classify 22 airport concessions as being priority in the Investment Partnerships Program (PPI) creates expectations for the coming year.

On May 14, Machado Meyer hosted the meeting of the Infrastructure Committee of Ibrademp (the Brazilian Institute of Business Law) to discuss the different views on airport concessions, lessons learned, challenges, and new opportunities. Marcelo Allain, an economist, partner of BR Infra Group and former member of the Secretariat of the Federal PPI, and David Goldberg, engineer and partner at Terrafirma, under the supervision of the coordinator of committee José Virgílio Enei, participated in the discussion.

The discussions were started based on the success of the 5th Round of Concessions, held in March and marked by exponential interest, auctions with fierce bidding, and participation by global operators. The removal of the restriction on the participation by groups already benefited by other airport concessions proved to be correct, and did not harm competitiveness, nor the success of new entrants such as the Spanish group Aena and the Brazilian group Socicam.

The model of the block concession, combining more profitable airports with smaller ones (“bone-in steak”), was also a viable alternative to not burden Infraero with only deficient airports, which opens space for its potential liquidation after the privatization of all the airports it administers.

The strategic (and ideological) error of keeping Infraero with a minority stake (49%) in the airports of the 2nd and 3rd rounds (Guarulhos, Viracopos, and Brasília; Confins and Galeão) was also discussed. Initially, the government left money on the table at the auction, selling only a 51% stake in airports at the height of market optimism. It ended up being penalized once again, as Infraero was obliged to bear the necessary investments and losses resulting from an actual demand much lower than what was originally projected. Given the low return of these airports and the limited rights of governance recognized for Infraero in the concessionaires, there is uncertainty about the value that it could obtain from the sale of these stakes.

Due to the precarious financial conditions of these first airports, the difficulty of effecting a consensual return is evident. Although Law No. 13,348/2016 has given legal authorization in this regard, the lack of regulations, especially as regards the criteria for indemnification for investments not amortized for the concessionaire that returns the asset, aggravates the scenario of uncertainty. The concern of the granting authority seems to be that if, on the one hand, the accounting criterion is more appropriate (and consistent with the letter of the law), as opposed to, for example, the asset or market replacement value, construction contracts with related or oversized parties may lead to discussions, especially with the supervisory bodies.

Some factors help explain the difficulties faced by airports for which concessions were granted in the first three rounds. One of them would be the frustration of demand, due to the greatest economic crisis ever experienced by Brazil. However, this fact has not been recognized in the administrative sphere as force majeure and, therefore, has not led to any economic and financial rebalancing of the contracts.

In addition, the significant bids offered in those rounds were translated into payments of fixed annual grants, increasing the risk of insolvency and pressure on the concessionaires’ cash. This risk has been mitigated in the most recent rounds, either because the most significant bids are payable at the time of the concession (lesser burden on future cash flow, especially if financed with equity), or because the concessionaires now have a grace period to start paying the annual grant installments.

The contractual rigidity of the first rounds was also pointed out, in which investments were required throughout the concession, regardless of the materialization of the demand estimated. This problem was once again corrected in the latest rounds, which conditioned investment obligations on certain demand triggers, as was already the case in road concessions.

Other factors further sharply deteriorated the economy of some of the first airports for which concessions were granted. The Viracopos concessionaire, for example, bet on a business model, freight transport, which did not materialize. With the development of new models of passenger aircraft capable of holding larger volumes of cargo, other airports eventually ended up gaining a share of that market.

Galeão Airport was impacted even more intensely by the Rio de Janeiro crisis and the frustration of demand, which was far below the national average. Finally, São Gonçalo do Amarante Airport (1st round) suffered due to the lack of access construction works for which the Rio Grande do Norte state government was in charge.

In an analysis of what the industry should expect in terms of new projects, a scenario was presented at the event based on some 600 public airports in Brazil, 10% of which are only under federal control, although they concentrate 95% of the passengers. Very few regional airports (of states or municipalities) would be eligible for concession or privatization without public subsidies or consideration, as in the public-private partnership (PPP) model. Even those that are theoretically self-sustaining could be subject to the granting of a concession for an investor profile very different from international operators interested in federal airports.

Regarding the 6th Concessions Round, announced by the federal government for 2020, it is already known that the block model will be maintained. Twenty-two airport concessions will be tendered, structured into three blocks: South, North, and Central. Per the profile of the assets, it is difficult to predict whether the result of this round will repeat the high bids of the prior one.

The Congonhas and Santos Dumont terminals ended up being included only in the 7th and last round of concessions. The strategy of keeping the crown jewels for the end was supposedly structured as a way to compensate investors for less attractive federal airports, in the logic of cross-subsidization of the blocks.

Over the years, the feeling that has resulted, therefore, is that the modeling of airport concessions has been evolving based on the successes and mistakes of past experiences. The balance is positive and the challenges to be faced are not few.

- Category: Labor and employment

"After undergoing various changes for approval by the Chamber of Deputies on August 13, 2019, the bill arising in response to the Economic Freedom Executive Order went to vote in the Federal Senate.

On August 21, 2019, the Federal Senate approved the text of the bill with the removal of one more point that impacted on labor and employment law: the authorization to work on Sundays and holidays.

Initially, the bill authorized work on Sundays and holidays, which payment must be remunerated at twice the usual amount (100% premium), unless a compensatory day off is granted to the employee, and the weekly rest must only be on a Sunday, once every four weeks.

Because of this exclusion, the rule for work on Sundays and holidays should remain as currently provided for by labor and employment law.

If the bill is signed, the labor law will have the following impacts:"

- Category: Infrastructure and energy

Signed into law by President Jair Bolsonaro with a partial veto, Executive Order (MP) No. 863/18 was converted on June 17th into Law No. 13,842, which extinguished the 20% limit on the participation of foreign capital in Brazilian airlines.

Aside from repealing the articles of the Brazilian Aeronautical Code (CBA) providing for a limit on foreign ownership of airlines and other requirements for their operation in Brazil, MP 863 reinstated the minimum baggage allowance per passenger, in opposition to Resolution No. 400 of the National Civil Aviation Agency (Anac), which authorized this charge starting in 2017. The allowance would be up to 23 kilograms for aircraft above 31 seats, up to 18 kilograms for aircraft from 21 to 30 seats, and up to 10 kilograms for aircraft of up to 20 seats. Only the excess could be charged separately.

The president, however, vetoed the articles with the final text related to the minimum baggage allowance, arguing that this topic was outside the purpose of MP 863, which was restricted to the participation of foreign capital in Brazilian airlines and, therefore, would violate the democratic principle and due process of law. Bolsonaro also argued that re-establishing the allowance runs counter to the public interest and does not benefit the air transport market, which needs more competition.

Since the publication of Resolution 400, airlines have been advocating charging as a way to lower the price of air tickets for consumers who travel with only one small carry-on bag. According to the airlines, the reduced ticket price plus the amount charged per bag would not exceed the amount to be paid for a ticket with a minimum baggage allowance included.

With the new rules, Brazilian companies come into compliance with the low-cost model existing abroad, which may increase the interest on the part of foreign investors in our air services market. As domestic competition increases, prices are expected to fall for end consumers.

For a complete review of the new rules for the industry, please review “Changes in the proposed opening of the capital of airlines to foreign investment.”

- Category: Banking, insurance and finance

Executive Order No. 881 (MP 881), issued on April 30 of this year, aims to ensure and foster economic freedom in Brazil, as well as reduce bureaucracy in various industries.

The principles that guide the text are: (i) presumption of freedom in the exercise of economic activities; (ii) presumption of good faith by private entities; and (iii) minimal intervention by the federal government in the economy. A practical example of these principles is that MP 881 expressly provides that that which is agreed upon by the parties prevails over regulations by the public order, with some specific exceptions.

Already in its article 1, the presidential decree reflects a liberal view of the law, in line with the basis of free enterprise, provided for in article 1, IV, of the Federal Constitution. As we shall see below, the text eliminates various formalities for business activity, including more stringent requirements in order to pierce the corporate veil.

MP 881, which should be read in conjunction with some infra-legal rules, ensures that individuals and legal entities are protected by a set of rights under the Federal Constitution, especially as regards private property and its social function, free competition, and encouragement of small businesses. Certain provisions of Law No. 10,406/2002 (the Civil Code), for example, have been amended to give greater legal certainty to contracts.

The presidential decree also amended article 421 of the Civil Code, stating that, in agreements between individuals, State intervention must be minimal. This makes any revision of contractual provisions an exception rather than a rule. This provision is relevant because it addresses the fact that Brazilian courts often adopt a broad interpretation of powers to revise contracts. For the same reason, the new article 480-A has been included in the Civil Code to allow parties to set objective parameters for revision of contracts and requirements for termination.

Article 480-B has also been included to establish that in commercial transactions it should be assumed that the parties had equal bargaining powers and that their allocation of risks should be respected. The aim is to avoid interpretation against the weaker party in business dealings and to restrict judicial revision of contracts.

For the investment fund segment, MP 881 brought in changes by introducing articles 1,368-C to 1,368-E in the Civil Code. The highlight is the limitation on liability of unitholders of funds and fiduciary service providers. The articles in question apply to all classes of investment funds, including those governed by CVM Instructions 555/14 and 578/16. Regarding the activities of fiduciary service providers, it is estimated that the changes brought in by MP 881 will encourage these agents to engage in the entire process of operations involving investment funds.

Presidential decrees have the same force as federal law, but are only effective for 60 days (extendable for another 60 days). During this period, the National Congress may (i) convert them into law, as originally written or amended; or (ii) reject them in their entirety, thus making them no longer effective.

MP 881 brings in significant advances related to economic activity as a whole. However, it is necessary to determine whether it will be converted into law and even then such provisions will still be subject to the Judiciary and regulations by public agencies.

- Category: Intellectual property

Last month the Brazilian Federal Senate approved the Legislative Decree Bill (PDL) No. 98/2019, regarding Brazil's accession to the Madrid Protocol and its Common Regulations, in order to facilitate the international registration of trademarks. The promulgation of the presidential decree on the agreement and the deposit of the accession instrument with the World Intellectual Property Organization (WIPO) are still pending.

In force since April of 1996, the Madrid Protocol has more than 104 signatory countries (which jointly represent 80% of the world economy)[1] and is administered by the WIPO, a UN agency focused on the international protection of intangible goods - notably trademarks, patents, industrial designs, and copyrights - and is responsible for publishing measures for this purpose, such as the treaty discussed in this article.

The agreement establishes the simultaneous international registration of trademarks, through a single deposit that may cover other applications to the remaining signatory countries. In Brazil, the application for trademark registration will be requested to the National Institute of Industrial Property (INPI), the governmental body responsible for forwarding it to the International Bureau of the WIPO. Thereafter, the WIPO will receive the notification and forward it to the other signatory countries for which the applications were originally claimed.

Likewise, if a foreign party wants to register its trademark in Brazil, it must apply to the industrial property office of its own country, which will send it to the WIPO and the same procedure will be adopted. The application examination will be carried out by the office of the member country of the filing for which registration is sought.

From a practical point of view, it is estimated that the Madrid Protocol will be in force in Brazil as of October of this year and its accession will bring benefits for individuals and legal entities, both foreign and domestic, among which we highlight:

- Cost reduction of administrative fees, as only one fee will be paid;

- Simplification of the trademark registration procedure, since a single deposit may be made with an indication of whether or not there is an intent to register the trademark in other countries; and

- Decrease in the time for review of applications, limited to 18 months. The average time for the INPI to review trademark applications was 24 to 48 months in 2017, and fell to 12 to 13 months in 2018. Currently, the INPI’s review takes an average of 11 months, which is in line with the content of the protocol. Backlog decrease was urged by Brazil's intention to accede to the Madrid Protocol.

The approval of the Madrid Protocol is undoubtedly a step forward in simplifying bureaucratic procedures and reducing costs related to international trademark protection, which will consequently boost the economy, making Brazil more competitive on the global scenario.

- Category: Capital markets

In late June the CVM (Brazilian Securities and Exchange Commission) published four new rules establishing a new regulatory framework for procedures related to sanctioning actions by the authority. The first of them was CVM Instruction No. 607, of June 18. A week later, it was followed by CVM Instructions No. 608 and No. 609, which update the framework and the values for punitive fines, consolidating the applicable values of fines into a unified standard, and CVM Resolution No. 819, which amends procedures applicable to appeals to boards of the body against decisions issued by its commissioners.

With the initiative, the CVM systematized previously sparse provisions in various resolutions and instructions into a single rule regarding sanctioning administrative proceedings within its purview. The following rules were repealed: (i) CVM Resolution No. 390/01, regarding the execution of Consent Orders; (ii) CVM Resolution No. 538/08, regarding sanctioning administrative proceedings; (iii) CVM Resolution No. 542/08, on the adoption of preventive and supervisory procedures in the scope of CVM's supervisory activity; (iv) CVM Resolution No. 552/08, on CVM Resolution No. 538/08; (v) CVM Resolution No. 775/17, regarding the simplified procedure for sanctioning administrative proceedings within the purview of the CVM; and (vi) CVM Instruction No. 491/11, on cases of serious infringement, pursuant to paragraph 3 of article 11 of Law No. 12,715/2012.

The systematization of the content related to sanctioning administrative proceedings within the purview of the CVM seeks essentially to adjust the regulations to the new rules established by Law No. 13,506/17, which, among other measures, increased the limit of the maximum penalty that may be applied by the CVM and introduced the administrative settlement in supervisory proceedings, reinforcing the regulatory framework for measures that may be used by the CVM as a securities market oversight body in Brazil. In addition, by means of CVM Instruction 607, the regulator sought to provide greater legal certainty to covered parties in relation to the procedures for the CVM's sanctioning actions.

In this manner, CVM Instruction 607 sought to clarify, simplify, and objectify, among other issues, the rules, procedures, and deadlines for the performance of procedural acts both by covered parties and by the CVM itself, its departments, and the Specialized Federal Prosecution Office. In addition, the new norm establishes objective parameters for the initiation of sanctioning proceedings and the dosimetry of the penalties that may be applied, by defining the base penalties, mitigating and aggravating conditions, and their impacts.

Some specific points which we will discuss below draw attention to these parameters and should be considered by the managers of public companies and other entities subject to the CVM’s supervision.

One of the main points of CVM Instruction 607 is the concern with complying with the command of paragraph 4 of article 9 of Law No. 6,385/76, as amended by Law No. 13,506/17, to the effect that the sanctioning actions of the body should prioritize infractions of a serious nature in order to provide greater educational and preventive effect for market participants.

In the same vein, the norm makes clear the discretion of CVM's departments so that they, considering the information obtained in the investigation of administrative infractions, may refrain from presenting a charging document when the conduct under investigation is of little relevance or the significance of the threat or harm to the legal goods protected by the rules infringed is low. It is at the discretion of the departments to also use other supervisory instruments or measures.

Although this is a subjective analysis by the CVM, the standard sought to establish the parameters that should be considered in this evaluation of the relevance of the conduct or significance of the harm, including: (i) the degree of reprehensiveness or repercussion of the conduct; (ii) the significance of the sums associated with the conduct; (iii) the significance of the losses caused to investors and other market participants; (iv) the impact of the conduct on the credibility of the capital markets; (v) the background and good faith of the persons involved; and (v) the reimbursement of the investors harmed.

Thus, while on the one hand the subjectivity of the assessment removes legal certainty from the covered parties, on the other the specification of the factors that must be taken into consideration allows covered parties and their attorneys to better define a defense strategy.

Another issue that draws attention in CVM Instruction 607 is the concern with making the procedures and procedural deadlines clear. In this sense, one sought to establish transparent and objective criteria for summons, presentation of charging documents, presentation of defenses, requests for the production of evidence, judgment of cases, appeals, production of effects of decisions, and other eminently procedural issues.

The counting of deadlines was unified and aligned with the rules of the Brazilian Code of Civil Procedure, thus reducing the divergence in understanding on the subject among the departments of the CVM. Henceforth deadlines shall be calculated exclusively in business days, excluding the first day and including the last day. Filings shall be considered valid until 11:59 pm of the last day of the deadline.

In a very efficient manner, the norm allowed the use of electronic means for the communication of the procedural acts of sanctioning administrative proceedings by establishing management and processing of cases exclusively via digital means and mentioning the requirements for the summons and subpoenas of the parties and for the counting of deadlines.

Such changes represent a gain in legal certainty for the covered parties to act in their defenses.

Another point that draws attention is the special focus on the principle of administrative law regarding the validation of administrative acts. The norm even allows the reformulation of charging documents when the requirements related thereto are not met. It also makes clear that absolute nullity of acts will be exceptional.

Also noteworthy is the application of confidentiality to administrative sanctioning proceedings, which will become the rule, contrary to the fundamental precept of law that administrative proceedings are public, and may proceed under seal on an exceptional basis. With the new rule, only the parties and their attorneys will have access to the record, and access by third parties should be evaluated by the reporting judge.

CVM Instruction 607 also established objective criteria for the dosimetry of penalties that may be applied by the CVM, which now have very high bases for pecuniary sanctions and with objectively defined mitigating and aggravating factors to guide the calculation of the final penalties. Thus, the norm gives greater predictability to penalties according to the type of conduct and its severity.

To set the base penalties for fines with a limitation criteria up to R$ 50 million (there are other criteria for setting the fine, such as three times the economic advantage obtained or twice the damage caused to investors, among others), the new rule establishes different values and limits depending on the nature of the infringement. To this end, the CVM divided administrative offenses into five large groups and established for each of them a maximum value for the base penalty. Below are some examples of conduct and the respective maximum values of the base monetary penalty:

- Group I (infractions related to the preparation and maintenance of the corporate books, failure to disclose periodic and occasional information, among others): R$ 300,000;

- Group II (non-disclosure or untimely disclosure of a material fact, non-preparation or preparation of periodic and occasional information not in compliance with regulations, among others): R$ 600,000;

- Group III (infractions related to the preparation of financial statements and non-compliance with the fiduciary duties of the audit committee, among others): R$ 3,000,000;

- Group IV (infractions related to the exercise of the voting rights of shareholders, directors and officers in a conflict of interest situation, among others): R$ 10,000,000; and

- Group V (infractions related to non-compliance with the fiduciary duties of directors and officers, abuse of control and voting rights, and use of information not yet disclosed to the market, among others): R$ 20,000,000.

Once the base penalty has been established, it is necessary to check for mitigating or aggravating circumstances. Each occurrence of a mitigating or aggravating circumstance will add to or reduce the base penalty by up to 25%.

Examples of aggravating circumstances are: (i) systematic or repeated performance of irregular conduct; (ii) high damage caused; and (iii) significant advantage obtained by the offender, among others. Examples of mitigating circumstances include: (i) confession to the offense or provision of information regarding its commission; (ii) the good record of the offender; (iii) reversion of the infraction; and (iv) effective adoption of internal integrity procedures and application of codes of conduct and ethics, among others.

The CVM board will also consider, for dosimetry of the penalty, any sanctions related to the same facts that have already been or will be applied by other authorities.

The new standard also includes procedural rules regarding Consent Decrees and Supervisory Settlements, established by Law No. 13,506/17.

The wording of CVM Instruction 607 implies that there will be a hardening on the part of the regulator with respect to the application of much higher penalties. Because of this, it is important to encourage effective adoption of internal integrity, audit, and reporting mechanisms and procedures, as well as effective application of codes of ethics and conduct within publicly-traded companies, as this is considered a mitigating circumstance in the application of the penalties provided for and may reduce them by up to 25%.

It is prudent, therefore, that publicly-traded companies and their directors and officers adopt a more proactive stance with respect to compliance with the CVM rules applicable to them by enhancing their corporate governance structures in order to prevent infractions.

CVM Instruction 607 enters into effect on September 1, 2019, and will be immediately applicable to ongoing proceedings, without prejudice to acts that have been performed thus far. CVM Instruction 608, in turn, will enter into force on January 1, 2020, and will apply to periodic or occasional information whose delivery period expires after its entry into force, as well as with respect to non-compliance with specific orders issued by the CVM after that date. Finally, CVM Instruction 609 also enters into effect on January 1, 2020, amending and adding provisions to various other instructions, including CVM Instruction 480/09, which sets forth the main periodic and contingent obligations applicable to publicly-traded companies in Brazil.

- Category: Real estate

Discussions on the issue of regulating the process of acquisition of rural real estate by foreigners should gain momentum following the presentation to the Federal Senate of Bill No. 2,963/19, dating from the end of May of this year. The text of the bill addresses various problems that the market faces with current laws and regulations, which depends on an extremely bureaucratic, uneven procedure and no operational resources for its implementation. All of this makes the acquisition process time consuming and affects the legal security of investment projects.

Until recently, the subject was being addressed under Bill No. 2,289/07, which, with its five other related bills, has been awaiting review by the Chamber of Deputies since September of 2015. Although discussions must now start at square one, a more up-to-date text may facilitate the approval process in the houses of the Legislature.

The main amendment proposed by Bill 2,963/19 is the treatment given to Brazilian companies controlled by foreigners. Currently, Brazilian companies directly or indirectly controlled by foreign individuals or legal entities are subject to the authorization procedure for acquisition of rural land provided for by law, as they are equated, for this purpose, to foreign companies.

According to the proposed text, Brazilian companies incorporated under Brazilian law will no longer be subject to any restrictions, except in certain specific and pointed cases. In other words, the proposed rule is of a general permission with exceptions instead of the current rule of general restrictions with specific authorizations.

Situations that will remain subject to restrictions, including those requiring approval by the National Defense Committee and regardless of whether the company is Brazilian, include the following: companies owned and controlled by sovereign wealth funds; foreign controlled companies when the property is located in the Amazon Biome and is subject to a legal reserve of 80% or more; and non-governmental organizations and private foundations funded by the same foreign person.

With the probable intent of addressing difficulties faced in the provision of public services, the bill proposes that such restrictions should not apply in the case of acquisition or possession intended for the execution or operation of a public service concession, permission, or authorization. The text expressly mentions the activities of generation, transmission, and distribution of electric energy as examples.

Another issue addressed by the text of the law is the problem faced by foreign creditors in foreclosing on fiduciary sales over rural property, when, in the second auction, the property is not sold and automatically remains under the creditor’s ownership. The law’s solution is to provide that, in such cases, ownership of the property must remain within the conditioned ownership of the creditor for two years, renewable for another two. During this period, the creditor will be required to dispose of the property to third parties, under penalty of returning the property to the original owner (that is, the guarantor).